Mergers and acquisitions transactions in Hermosa Beach require thorough investigation before closing. Poor preparation leads to costly surprises that can derail deals worth millions.

At Pierview Law, we guide clients through comprehensive mergers acquisitions due diligence processes. Smart buyers examine every aspect of target companies to protect their investments and avoid legal complications.

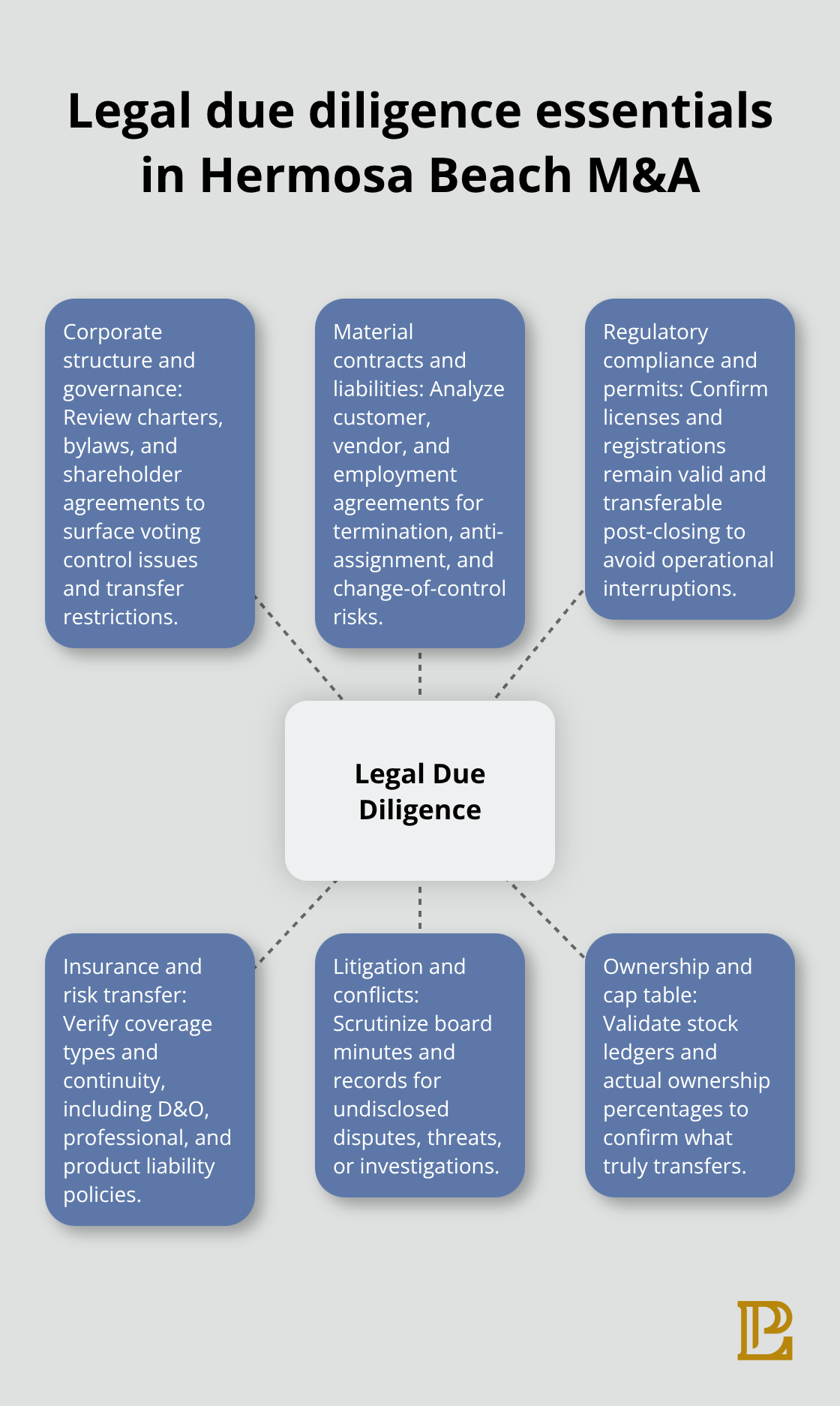

Legal Due Diligence Process

Corporate Structure and Governance Review

Corporate structure examination reveals ownership complexities that destroy deals. Delaware corporations with multiple share classes create voting control issues that buyers miss until closing approaches. We examine articles of incorporation, bylaws, and shareholder agreements to identify anti-dilution provisions and drag-along rights that transfer with acquisitions. Stock ledgers show actual ownership percentages, while board meeting minutes reveal undisclosed conflicts or pending litigation threats.

Contract Analysis and Liability Assessment

Material agreements require immediate attention during legal review. Customer contracts contain termination-for-convenience clauses that eliminate 40% of projected revenue overnight. Employment agreements with key personnel include golden parachute provisions that trigger during ownership changes (creating unexpected costs that average $2.3 million for mid-market transactions according to PwC research). Vendor contracts with anti-assignment clauses force renegotiation of favorable pricing terms. Insurance policies need coverage verification for professional liability, product liability, and directors-and-officers protection that transfers to new ownership.

Regulatory Compliance and Permit Verification

Business licenses and permits determine operational continuity post-acquisition. California businesses require specific state registrations that expire during ownership transitions, while federal contractors need security clearances that don’t automatically transfer. Environmental compliance records show potential EPA violations that create cleanup liabilities (averaging $1.8 million per incident). Professional service firms must verify individual practitioner licenses remain valid under new ownership structures, as medical practices and law firms face automatic license suspensions during corporate changes.

Financial analysis builds on these legal foundations to reveal the true economic picture of target companies. Experienced legal counsel becomes invaluable when navigating the complex legal landscape of mergers and acquisitions.

Financial Due Diligence Requirements

Financial Statement Analysis and Audit Review

Financial statements hide the reality behind acquisition targets. GAAP accounting allows revenue recognition manipulation that inflates performance by 15-30% according to Ernst & Young research. We examine three years of audited statements alongside management letters that reveal internal control deficiencies. Unaudited monthly financials show seasonal patterns and cash conversion cycles that annual reports obscure. Revenue concentration becomes apparent when single customers represent over 20% of total sales (creating dependency risks that destroy valuations overnight).

Cash Flow and Revenue Stream Evaluation

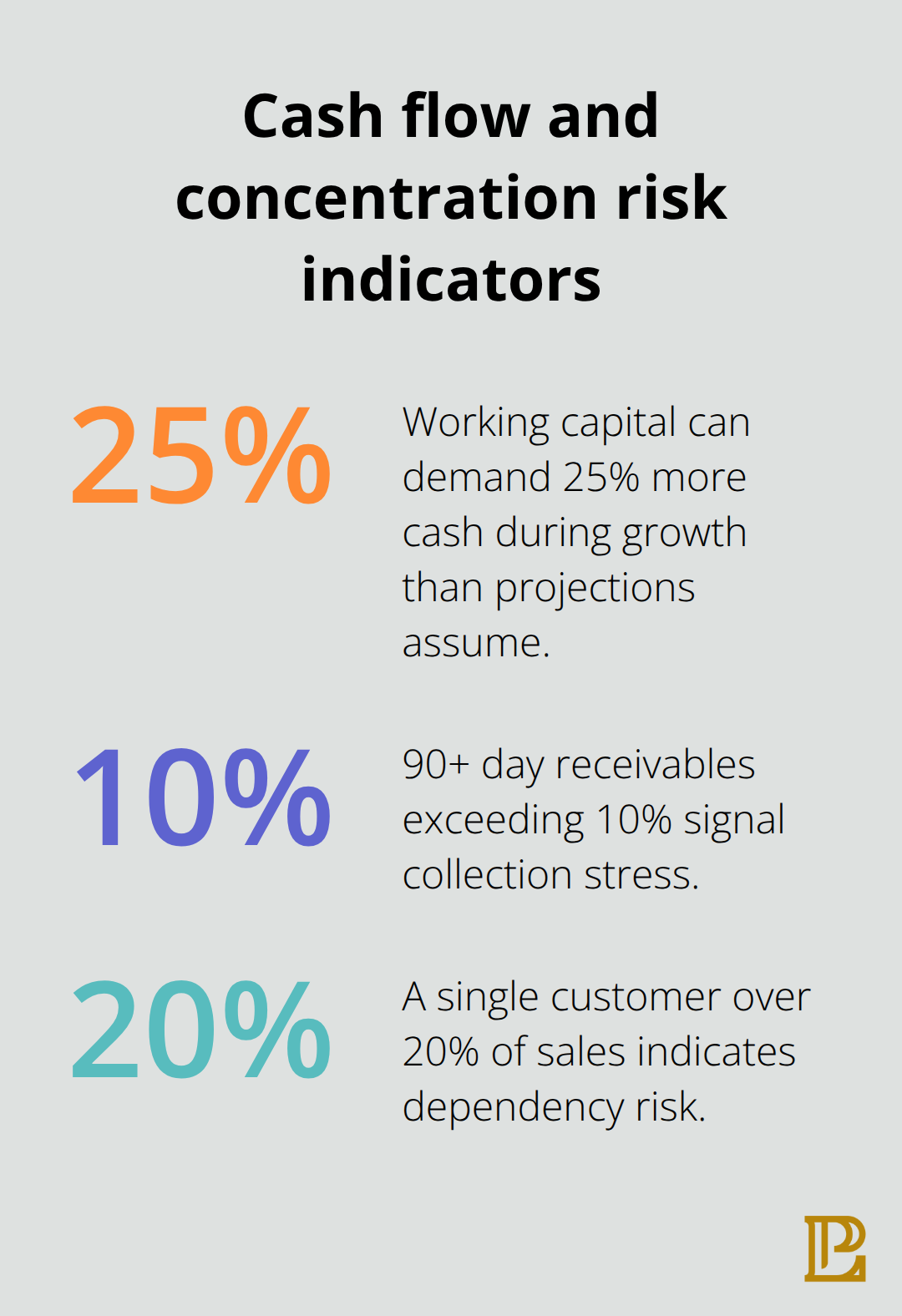

Cash flow analysis exposes operational weaknesses that income statements conceal. Working capital requirements consume 25% more cash during growth periods than financial projections indicate. Accounts receivable aging reports show collection problems when 90+ day receivables exceed 10% of total outstanding balances. Revenue streams require verification through customer contracts and payment histories to identify recurring versus one-time income sources.

Debt Structure and Working Capital Assessment

Debt covenants in credit agreements trigger acceleration clauses during ownership changes (forcing immediate repayment of outstanding balances). Bank reconciliations reveal cash management issues, while debt schedules show balloon payments that require refinancing within 24 months. California businesses face additional complexity with state tax obligations that create liens against assets during ownership transitions. Working capital analysis identifies seasonal cash needs and inventory turnover rates that affect post-acquisition operations.

Operational factors complement financial analysis to reveal how target companies actually function in their markets.

Operational Due Diligence Considerations

Business Model and Market Position Analysis

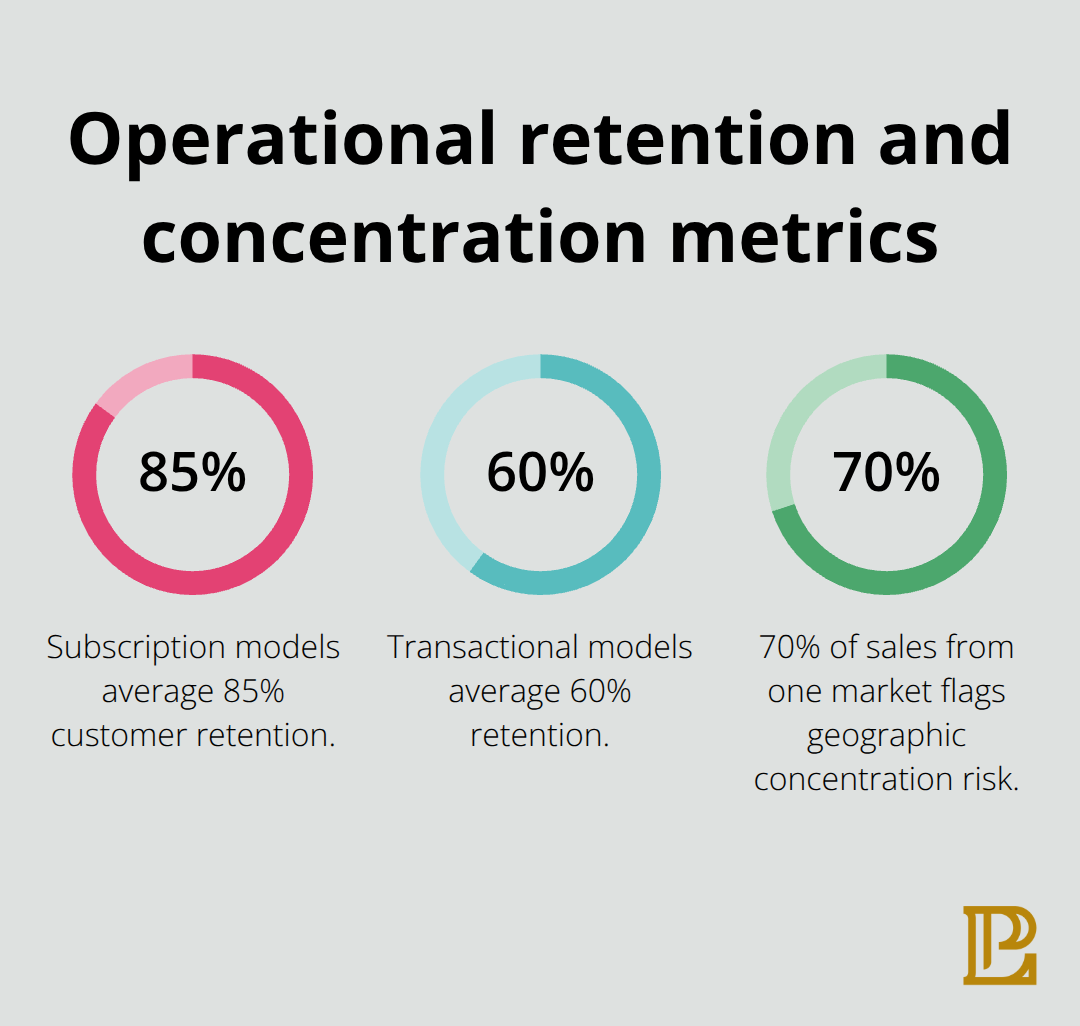

Business model evaluation starts with customer concentration analysis that reveals fatal dependencies. Companies with single customers representing over 30% of revenue face immediate risk when those relationships terminate post-acquisition. Subscription-based businesses show 85% customer retention rates compared to 60% for transactional models according to McKinsey research, which makes recurring revenue streams worth premium valuations. Geographic concentration creates additional vulnerability when 70% of sales originate from single markets that face economic downturns or regulatory changes.

Market position assessment examines competitive advantages and barriers to entry that protect revenue streams. Companies without proprietary technology or exclusive distribution agreements lose market share within 24 months of acquisition completion. Brand recognition studies reveal customer loyalty metrics that predict post-acquisition performance, while pricing power analysis shows margin sustainability under new ownership structures.

Key Personnel and Management Team Review

Key personnel retention becomes the primary operational concern during ownership transitions. Management teams with average tenure under three years lack institutional knowledge that maintains customer relationships and operational efficiency. Employment contracts without non-compete clauses allow departing executives to establish competing businesses that capture existing customer relationships within 18 months.

Compensation structures that rely heavily on equity incentives lose effectiveness during acquisitions and require immediate restructuring (costing 15-25% of annual payroll according to Deloitte studies). Technical leadership positions in software companies command 40% salary premiums during retention negotiations, while sales management departures reduce revenue by 20% within the first year.

Technology Systems and Infrastructure Evaluation

Legacy technology systems create integration nightmares that destroy acquisition timelines and budgets. Custom software applications without documentation require complete rebuilds that cost $500,000 to $2 million for mid-market companies. Cloud infrastructure assessments reveal security vulnerabilities and compliance gaps that trigger regulatory investigations during ownership changes.

Data migration projects from on-premise systems to cloud platforms take 6-12 months longer than projected timelines, while software licensing agreements contain change-of-control provisions that double annual costs. Cybersecurity audits identify network vulnerabilities that create liability exposure (averaging $4.35 million per data breach according to IBM research). System integration costs often exceed initial estimates by 40-60% when target companies operate incompatible platforms during mergers and acquisitions.

Final Thoughts

Successful mergers and acquisitions due diligence demands systematic execution across legal, financial, and operational domains. Buyers must start corporate structure analysis within 48 hours of letter of intent execution to identify deal-breaking issues early. Financial statement verification takes 30-45 days when teams conduct proper analysis, while operational assessments run parallel to avoid timeline delays.

The biggest mistake buyers make involves contract analysis shortcuts to meet closing deadlines. Anti-assignment clauses and change-of-control provisions destroy 25% of projected synergies when teams discover them late in the process (creating unexpected costs that average $2.3 million for mid-market transactions). Revenue concentration analysis gets overlooked until customer departure notices arrive post-closing.

Technology integration planning starts during due diligence, not after acquisition completion. Legacy system compatibility issues add 6-12 months to integration timelines when identified late. We at Pierview Law guide Hermosa Beach businesses through comprehensive mergers acquisitions due diligence processes that protect acquisition investments and contact our team for experienced legal counsel.