Your intellectual property is often your most valuable business asset, yet many business owners in Hermosa Beach overlook protecting it with proper insurance coverage.

At Pierview Law, we’ve seen firsthand how a single lawsuit or infringement claim can devastate a company that lacks adequate intellectual property insurance coverage. The right policy can be the difference between staying in business and facing financial ruin.

What IP Insurance Actually Covers

Understanding the Basics of IP Insurance

Intellectual property insurance is a custom-built policy that pays for defense costs, settlements, and damages when someone sues you for infringing their patents, trademarks, copyrights, or trade secrets. Unlike general business insurance, IP policies adapt to your specific portfolio and risk profile. The American Intellectual Property Law Association reports that the average cost of patent litigation alone exceeds $2 million through trial, with trademark disputes running $300,000 to $500,000. IP insurance absorbs these staggering legal bills before they drain your cash flow.

The policy typically covers your attorney fees, expert witness costs, court costs, and any settlement or judgment amount up to your policy limit. Some policies also reimburse you for pulling infringing products off the market or defending against counterclaims. When a third party alleges you’ve stolen or misused their IP, you file a claim and the insurer pays your defense costs from day one. This matters because e-discovery alone in a trademark case can cost $100,000 or more, and you cannot afford to wait for a judgment to get help.

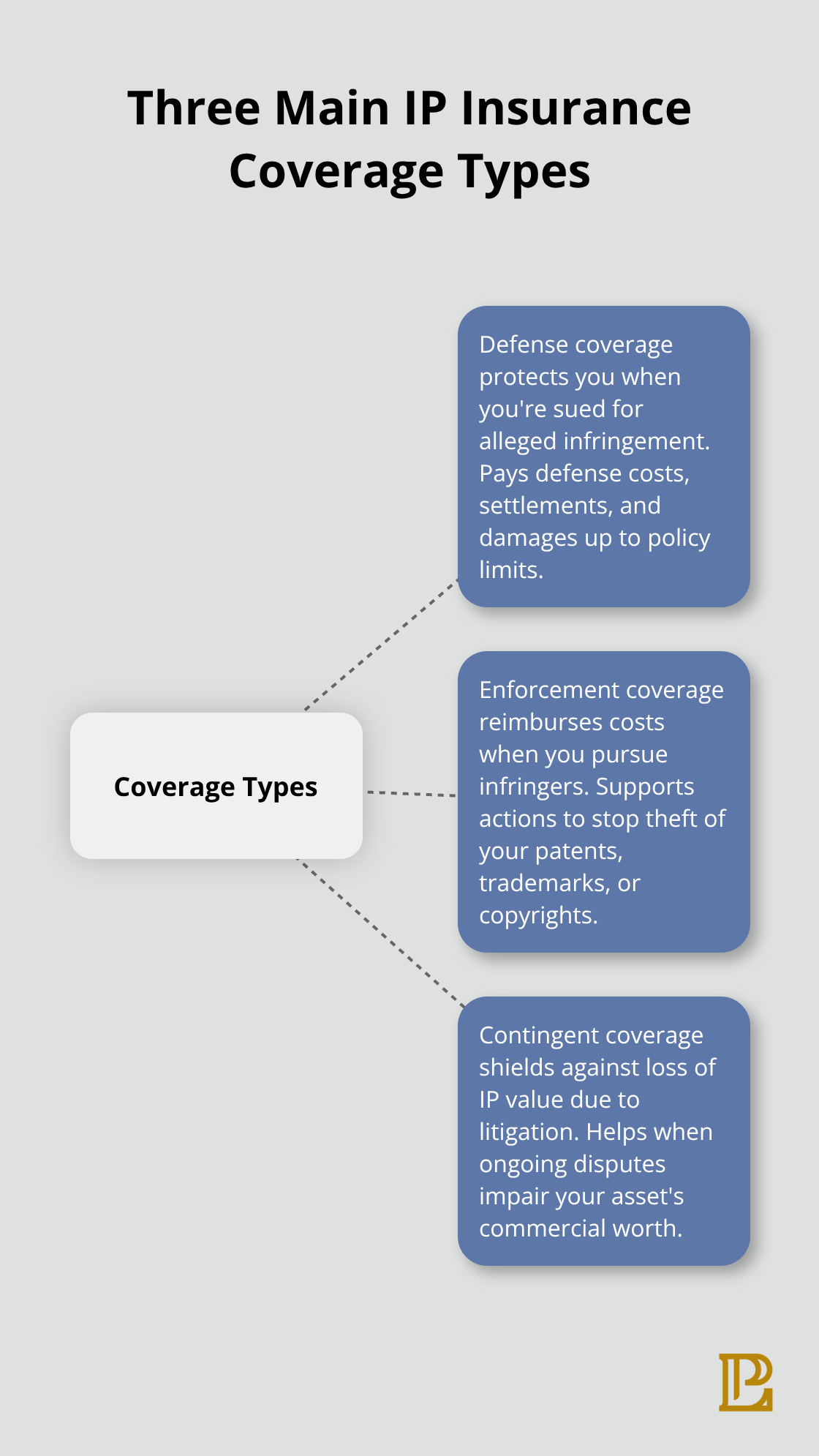

Three Main Coverage Categories

The coverage options break into three main categories. Defense coverage protects you when someone sues claiming you infringed their IP-the most common and affordable form. Enforcement coverage is the opposite: it reimburses your costs when you pursue someone else for stealing your trademarks, patents, or copyrights. Contingent coverage brackets catastrophic risk by covering losses if ongoing litigation destroys the value of your own IP assets.

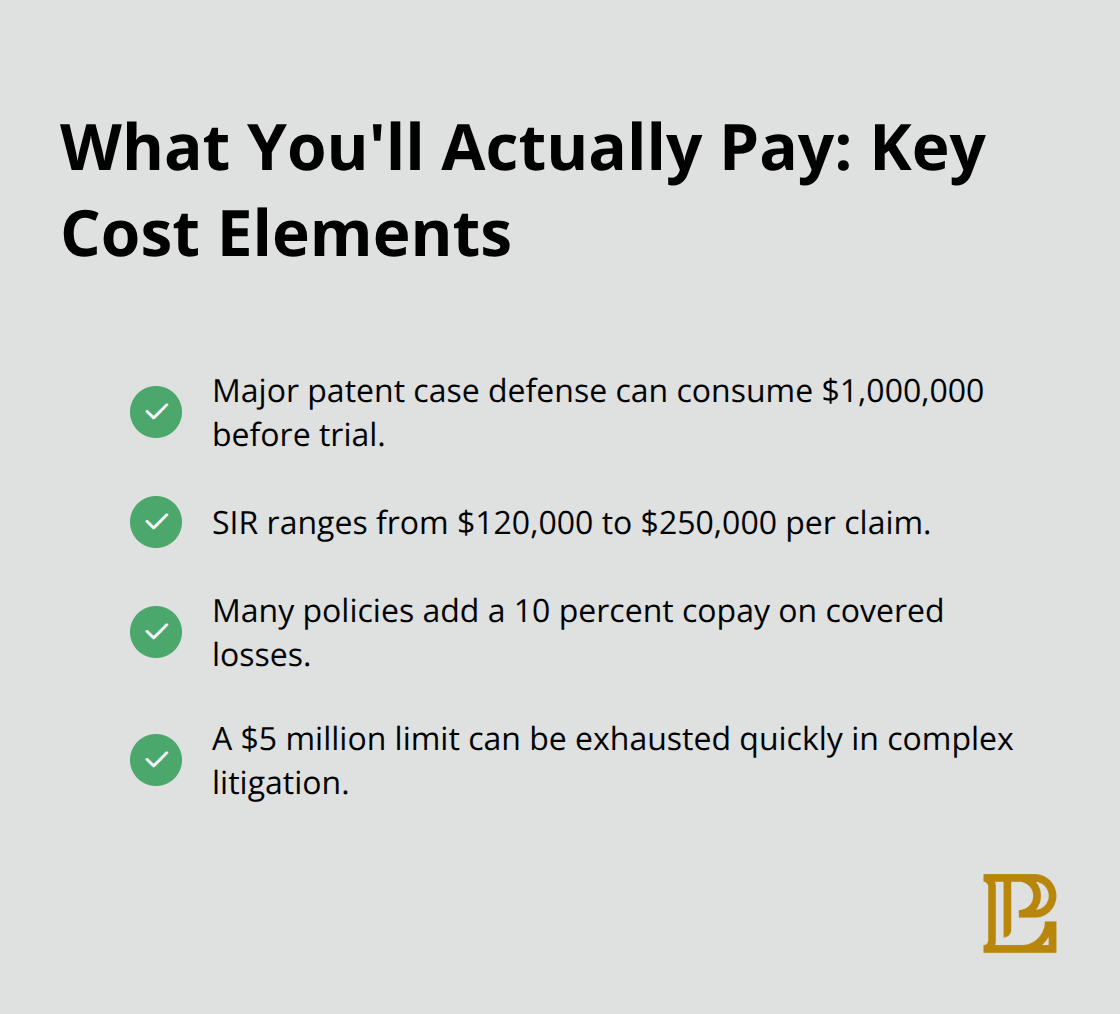

You can also layer on riders for data breach liability, breach of contract claims tied to IP licenses, or multi-peril coverage. The Self-Insured Retention, or SIR, is your out-of-pocket threshold before insurance kicks in; typical IP policies carry SIRs between $120,000 and $250,000 per claim, plus a 10 percent copay on covered losses.

What You’ll Actually Pay

Premiums vary wildly depending on your revenue, the size of your IP portfolio, and whether you license IP to others. A small Hermosa Beach business with a narrow product line and basic trademark protection might pay $5,000 to $10,000 annually, while a tech company with patents, software copyrights, and aggressive licensing could pay $50,000 or more.

IP insurance exists because courts award massive damages. When Honeywell sued Litton Industries over patent infringement, the verdict reached $1.2 billion. Polaroid’s case against Kodak resulted in a $900 million judgment. These are not hypothetical scenarios-they happen to real companies, and they can happen to you. Understanding what triggers coverage and how to structure your policy for your specific IP assets becomes the next critical step in protecting your business.

Choosing the Right Coverage for Your IP Portfolio

Build a Complete Inventory of Your IP Assets

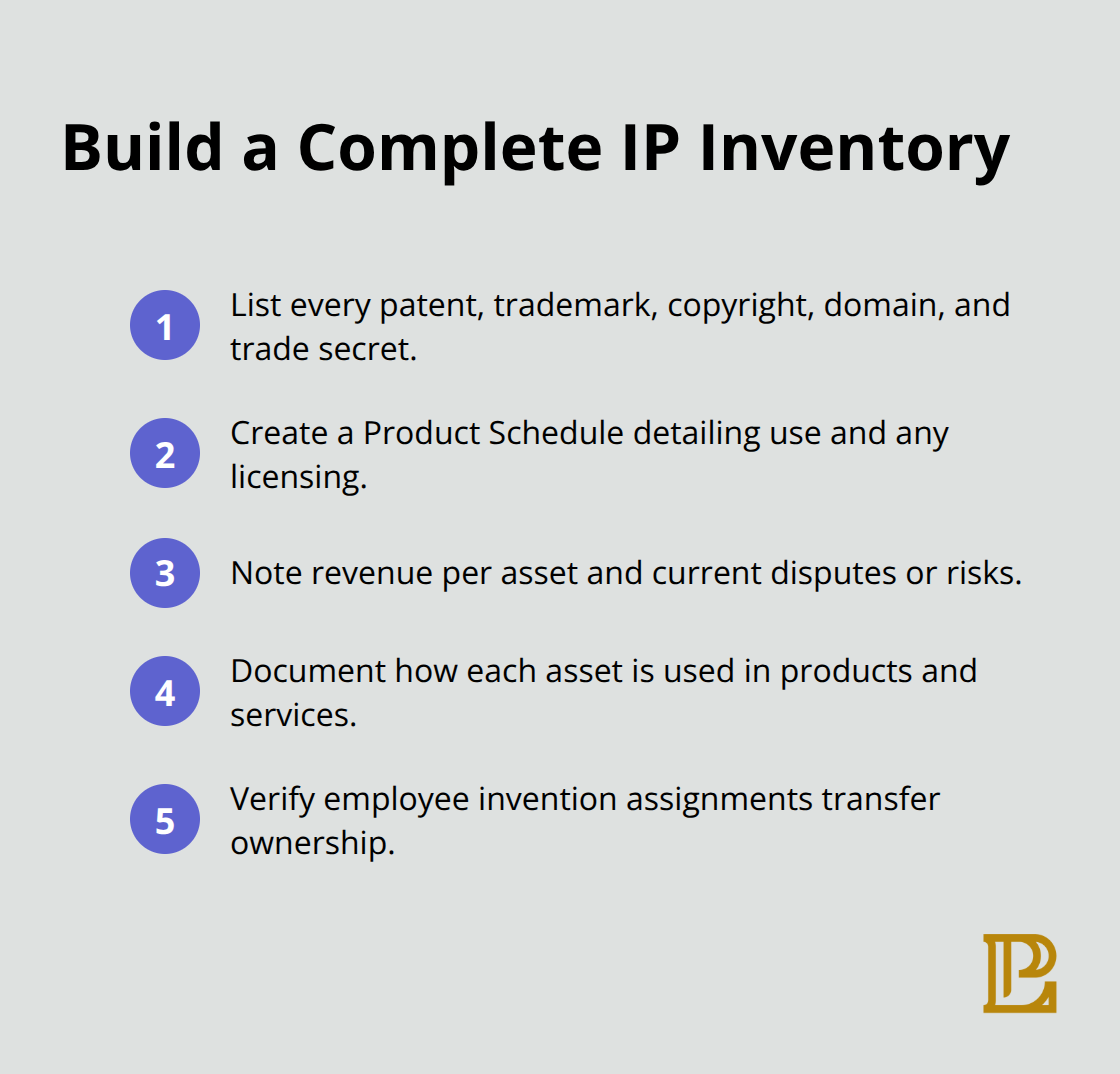

Start with a complete inventory of what you actually own. List every patent, trademark, copyright, domain name, and trade secret your business relies on. This step is not optional-it forms the foundation for everything that follows. When you apply for IP insurance, the insurer will request a Product Schedule that details each asset, how you use it, and whether you license it to others.

If you skip this step or provide incomplete information, you create coverage gaps that surface only when you need the policy most.

A software company in Hermosa Beach with patents on its core algorithm but no mention of that patent in the application might discover later that the algorithm isn’t actually covered. The insurer will want to know the revenue these assets generate, which ones face the highest infringement risk, and whether any are already under dispute. Take time to document this now. If you have employees, verify that your invention assignment agreements actually transfer IP ownership to your company. The Mattel v. MGA Entertainment case in the Ninth Circuit shows how ownership disputes can spiral into costly litigation when assignments are vague or missing. Courts weigh what your company actually contributed to developing the IP, and unclear terms invite challenges that your insurance won’t cover if the dispute centers on ownership rather than infringement.

Evaluate Your Industry Risk and Licensing Practices

Next, assess your actual risk exposure by looking at your industry, your competitors’ behavior, and your licensing practices. If you license IP to customers, that creates enforcement risk-you may need to sue licensees for breach or unlicensed use, which is why some policies include enforcement coverage alongside defense. The American Intellectual Property Law Association reports that trademark disputes average $300,000 to $500,000 in defense costs, while patent cases often exceed $2 million.

If your business operates internationally or your products are distributed across state lines, you face higher infringement risk because more potential competitors can access your market. A company selling software nationwide encounters more IP challenges than one serving only Hermosa Beach clients. When you meet with a broker or attorney to discuss coverage, bring your revenue figures, the number of employees involved in creating IP, and details about any prior disputes or cease-and-desist letters you’ve received. Be honest about this history-carriers use it to set premiums and identify exclusions.

Understand Policy Limits and Out-of-Pocket Costs

Finally, understand what policy limits actually mean. A $5 million limit sounds substantial until you realize that in a major patent case, defense costs alone can consume $1 million before trial even starts. The Self-Insured Retention (SIR) of $120,000 to $250,000 per claim means you pay that amount out of pocket before insurance begins. A 10 percent copay on top applies to many policies as well.

If your company has limited cash reserves, a high SIR makes the policy nearly worthless because you cannot afford to pay the threshold. Negotiate the SIR down if possible, especially if you have multiple products or licenses that might trigger separate claims in the same year. Once you understand your assets, your risk profile, and your financial capacity to absorb losses, you can move forward to identifying which specific coverage types actually match your business model and competitive position.

Gaps That Cost More Than You Think

Underestimating Your IP’s Real Value

Most business owners in Hermosa Beach drastically undervalue their intellectual property when shopping for insurance. You own a trademark worth tens of thousands of dollars in brand recognition, patents that took years to develop, or software code that represents your competitive advantage, yet you describe it vaguely on the insurance application as simply a product line. This vagueness creates the first major problem: inadequate coverage limits that sound reasonable until you face actual litigation.

When the American Intellectual Property Law Association reports that patent cases average $2 million in defense costs, a $1 million policy limit evaporates instantly once expert witnesses, discovery, and trial preparation begin. You end up paying the difference out of pocket, which means your company absorbs $500,000 or more in uninsured costs.

Hidden Exclusions That Leave You Exposed

Many policies exclude specific infringement scenarios entirely, and business owners never discover these gaps until they file a claim. A trademark policy that excludes counterfeit goods disputes leaves you defenseless against the exact threat you face if your brand is copied overseas. A patent policy that excludes declaratory judgment actions means you cannot defend yourself if a competitor sues first, claiming your patent is invalid.

These exclusions often hide in subsections of dense policy language that few people actually read before signing. The policy language intersects with post-grant proceedings and other patent law changes, creating traps that catch companies off guard when disputes arise.

Inventory Your Assets With Dollar Values

Work with a business attorney to list every IP asset your company owns, along with the revenue each asset generates and whether you license it to others. This forces you to assign real dollar values instead of guesses, which in turn drives appropriate coverage limits. Include patents, trademarks, copyrights, domain names, and trade secrets in your Product Schedule.

Document how you use each asset and whether any are already under dispute. If you have employees, verify that your invention assignment agreements actually transfer IP ownership to your company. The Mattel v. MGA Entertainment case in the Ninth Circuit shows how ownership disputes can spiral into costly litigation when assignments are vague or missing.

Negotiate Exclusions and Add Riders

Demand that the insurer’s broker walk you through the specific exclusions in plain language and explain how each one affects your actual business model. If the policy excludes declaratory judgments but your industry faces frequent validity challenges, negotiate to add that coverage back as a rider, even if it costs more.

Consider whether you need enforcement coverage to pursue infringers, contingent coverage to bracket catastrophic losses, or riders for data breach liability and breach of contract claims tied to IP licenses. The Self-Insured Retention (SIR) of $120,000 to $250,000 per claim means you pay that amount out of pocket before insurance begins, so negotiate the SIR down if your cash reserves are limited.

Schedule Regular Policy Reviews

Schedule a policy review every two years, particularly if you develop new products, launch new patents, or expand into new markets. An IP insurance policy that protected you adequately in 2023 may leave dangerous gaps in 2025 if your business has grown. Changes in your IP portfolio or new patents can lower premiums and improve coverage alignment, so keep your Product Schedule current to facilitate smoother renewals and catch exclusions before they harm you.

Final Thoughts

Selecting the right intellectual property insurance coverage requires you to know what you own, understand your actual risk, and negotiate terms that match your business reality. The American Intellectual Property Law Association data shows patent cases exceed $2 million in defense costs, trademark disputes run $300,000 to $500,000, and e-discovery alone can cost $100,000 or more. A policy limit that sounds adequate on paper disappears quickly once litigation begins, leaving you to absorb the difference from company cash flow.

Your next move is to schedule a conversation with a business attorney who understands both your IP portfolio and your financial capacity to absorb losses. Walk through your Product Schedule line by line, assign real dollar values to each asset, and demand that exclusions be explained in plain language rather than legal jargon. Negotiate the Self-Insured Retention downward if your cash reserves are limited, and consider whether enforcement coverage, contingent coverage, or riders for data breach and breach of contract liability make sense for your specific business model.

Contact Pierview Law to discuss your intellectual property insurance coverage needs and whether your current protection has gaps. Our team works with business owners throughout Hermosa Beach to structure IP insurance that actually protects what matters most to your company.