A bad title can tank your real estate investment before you even close the deal. Title underwriting in California practice protects you from hidden liens, ownership disputes, and other defects that could cost thousands to fix later.

At Pierview Law, we’ve seen investors lose money because they skipped proper title examination. This guide walks you through what title risk looks like, how underwriting catches problems, and the steps that separate successful investors from those who learn expensive lessons.

What Title Defects Actually Cost You in California

Unknown Liens and Public Record Errors

Unknown liens on a property represent the most frequent title problem in California transactions, and they hit your wallet hard. A contractor lien, judgment lien, or unpaid property tax can block the entire sale or force you to pay off the debt at closing, sometimes without warning. A thorough title review before you commit to a purchase catches these problems early and prevents costly surprises.

Errors in public records also plague California deals more often than investors realize. Misspelled names, incorrect property descriptions, or recording mistakes delay closing by weeks or even months. These errors require correction through the title company or an attorney before you can transfer ownership, adding time and expense to your transaction.

Boundary Disputes and Survey Issues

Boundary and survey disputes arise regularly in high-value markets like Hermosa Beach, where overlapping property descriptions or outdated surveys create real conflict. A licensed surveyor can clarify property lines and prevent costly disputes after closing. In markets where land values command premium prices, a boundary problem can derail your entire investment strategy.

Hidden Ownership Claims and Unreleased Liens

Undiscovered heirs or ownership claims can surface months or years after you close, leaving you vulnerable to loss of the property itself. Unreleased mortgages and easements linger on title even after payoff, and many buyers discover them only when title insurance is required by their lender. These issues are not theoretical-they happen in real transactions, and they cost real money to fix.

How Title Problems Shrink Property Value

A defective title directly reduces what your property is worth and what you can borrow against it. Lenders will not fund a purchase if the title carries unresolved liens or clouds, which means you lose financing options and negotiating power. In high-value Hermosa Beach properties, where land values already command premium prices, a title defect can wipe out tens of thousands in equity or force you to renegotiate the purchase price downward.

Title Insurance: Your Backward-Looking Protection

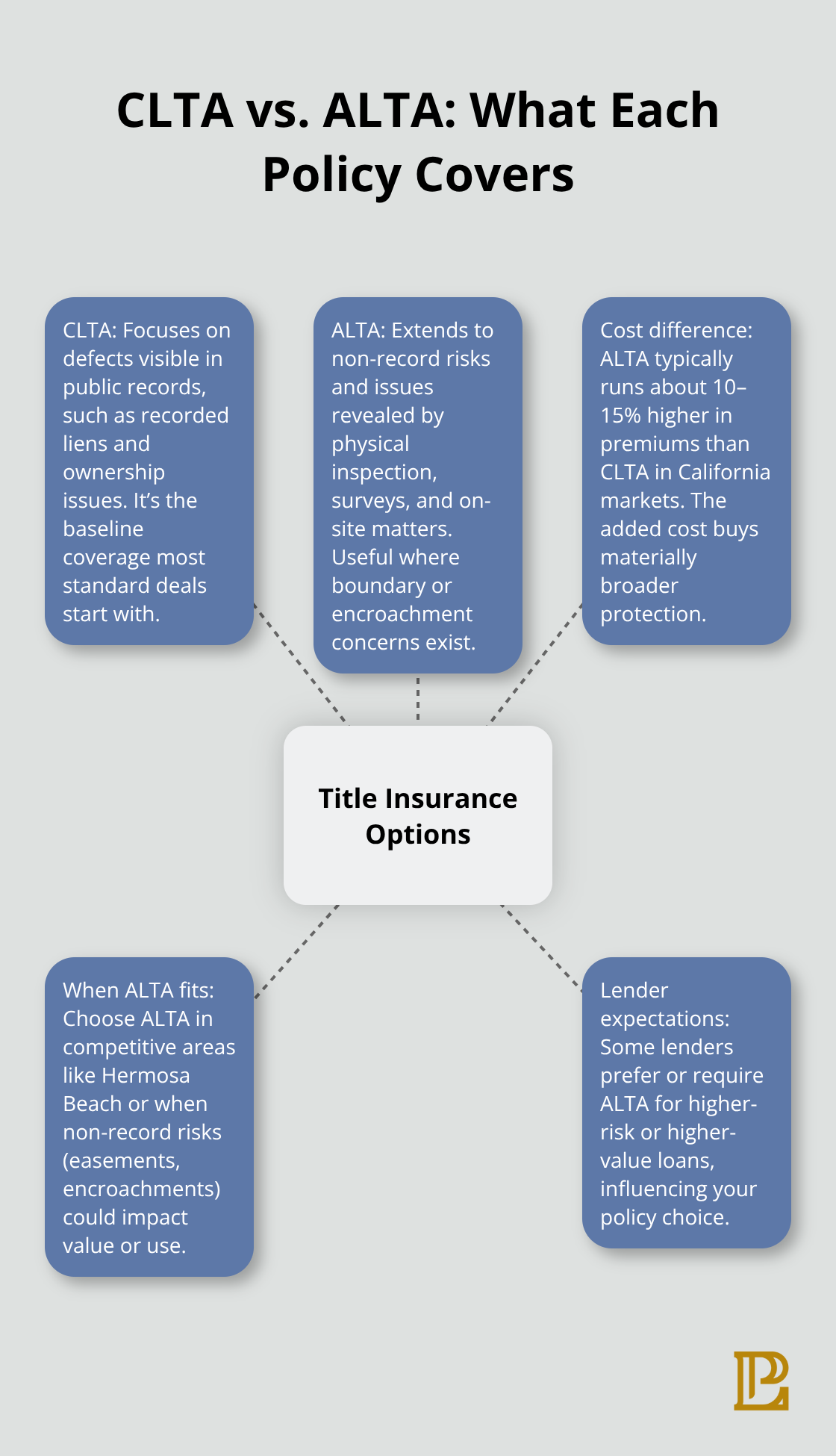

Title insurance protects you against defects that existed before you bought but were not discovered until after closing. California offers two main title insurance options: CLTA policies cover defects found in public records, while ALTA policies extend protection to issues revealed through physical inspection and matters outside the public record. ALTA coverage costs more but provides substantially broader protection in markets where non-record risks matter (such as boundary disputes or undisclosed easements).

For investors purchasing in California, particularly in competitive markets where the extra protection justifies the premium, ALTA coverage offers the security you need. The choice between CLTA and ALTA shapes your risk exposure for the entire time you own the property. Understanding which policy fits your real estate purchase sets the foundation for the underwriting process that comes next.

How Title Underwriting Protects Your California Investment

The Title Search: Foundation of Underwriting

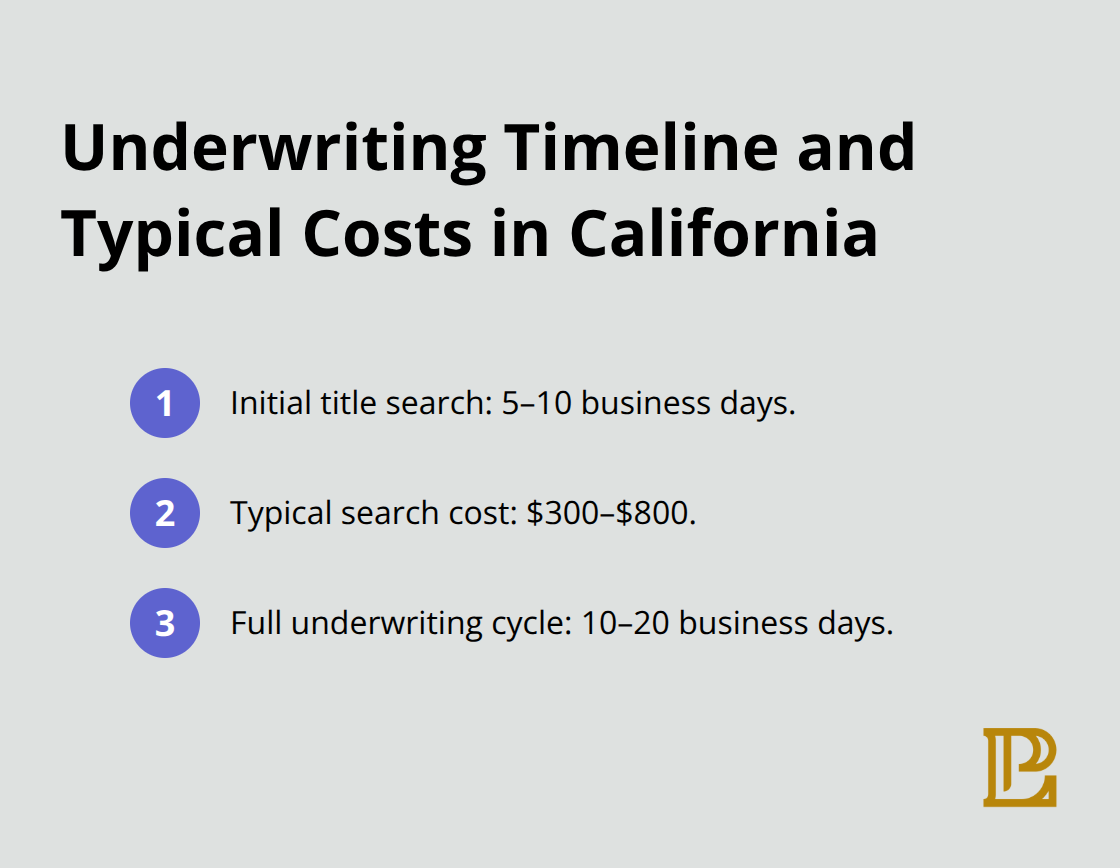

The title underwriting process in California starts with a comprehensive search that goes far beyond a quick records check. A title company pulls documents from the county recorder’s office, tax assessor records, and judgment lien databases to build a complete ownership history. This search typically takes five to ten business days and costs between $300 and $800 depending on property complexity and location. For Hermosa Beach properties, where land values run high and transaction stakes are significant, this investment pays for itself the moment it catches a problem that would otherwise derail your deal. The search uncovers liens, easements, deed restrictions, and ownership gaps that could affect your ability to use or refinance the property.

Reading and Resolving the Preliminary Title Report

Once the title company completes the initial search, they prepare a preliminary title report that lists every issue found on record. This report is not a guarantee of title-it is an offer to issue insurance once problems are resolved. California Insurance Code section 12414.30(b) makes clear that a preliminary report carries no binding obligation; it simply tells you what needs fixing before closing. You and your attorney review the report carefully. If the report shows an unpaid property tax lien, a contractor’s claim, or an old mortgage that was supposedly paid off, the title company works with the seller to obtain releases or satisfactions from the lien holders.

This is where many deals either move forward smoothly or stall completely. Some title issues resolve in days; others take weeks. A judgment lien against the seller might require a payment from sale proceeds to clear. An old easement might need clarification from the easement holder or a boundary survey to determine if it actually affects your intended use. The underwriting team assesses whether each issue is fatal to the transaction or manageable with proper documentation and insurance exceptions.

Lender Requirements and Extended Underwriting

Underwriting standards in California require lenders to approve title before they will fund the loan, which means your lender’s requirements drive much of the underwriting timeline. Most lenders demand a clear title report with no material liens or ownership defects before they will issue a loan commitment. If your lender requires ALTA coverage rather than CLTA, the title company conducts a more thorough examination that includes physical inspection of the property and review of zoning records, permits, and other non-record matters. This extended underwriting adds two to five days but catches issues that a records-only search would miss.

Final Approval and Closing Preparation

The final underwriting approval comes when the title company issues a title insurance commitment that lists all remaining exceptions (matters the insurance will not cover). You review this commitment carefully with your attorney to confirm that every exception is acceptable or has been resolved. Once you and your lender sign off on the commitment, the title company schedules closing and prepares final title insurance policies. In Hermosa Beach transactions, where properties often carry complex ownership histories or multiple easements related to coastal access or utility rights, thorough underwriting prevents post-closing disputes that could cost far more than the upfront title work. The entire underwriting process typically runs ten to twenty business days from initial search to final approval, depending on how quickly title issues surface and resolve.

With title underwriting complete and your insurance commitment in hand, you move into the final phase where proper documentation and coordination between all parties determines whether your closing happens on time and without surprises.

Preparing for Title Underwriting Without Surprises

Start Early to Avoid Last-Minute Problems

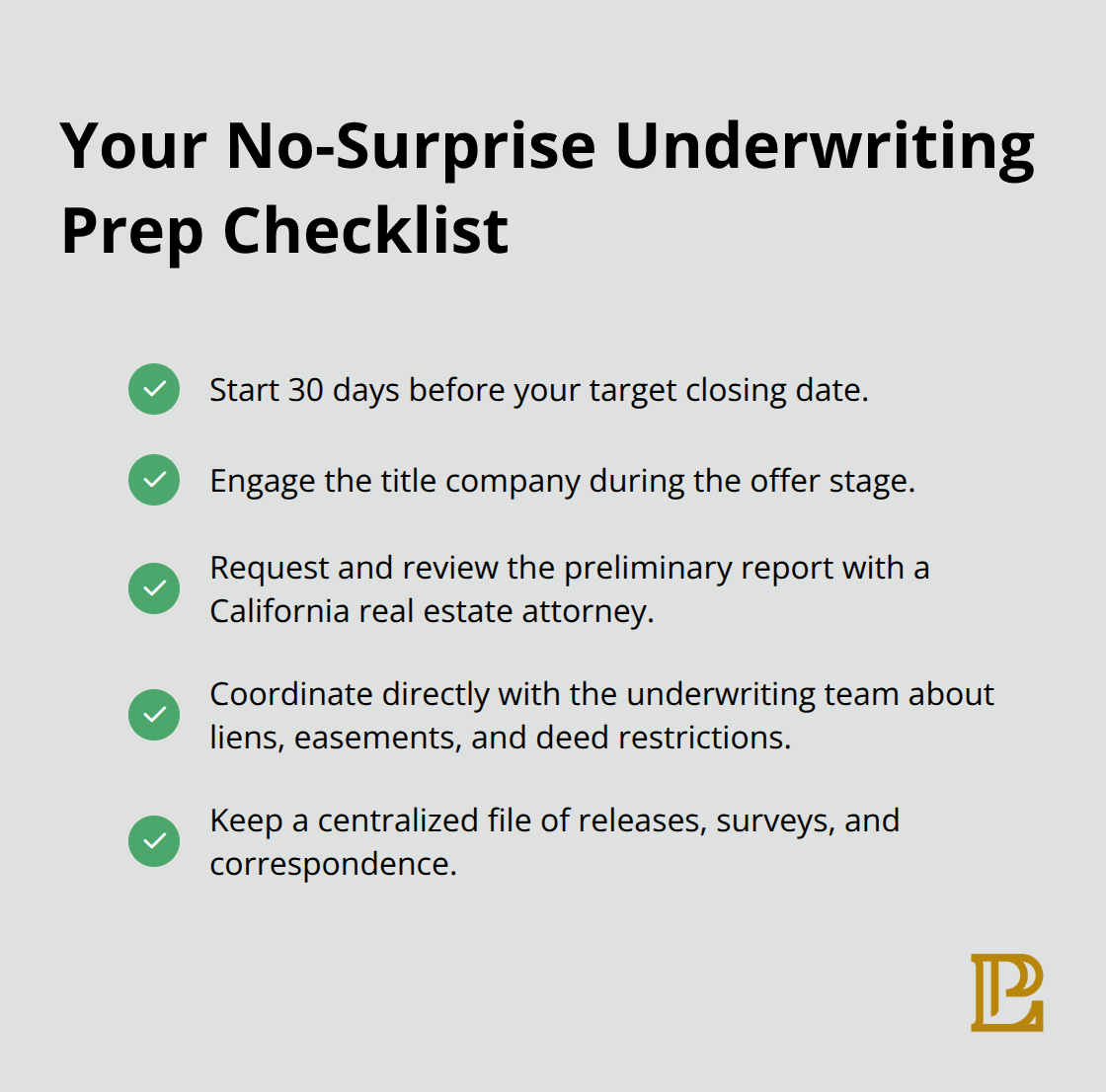

Title underwriting requires time that most investors underestimate. Contact your title company at least thirty days before your target closing date, not two weeks before. Most California title companies need five to ten business days just to complete the initial search, and you’ll need additional time to resolve any issues that surface.

If you’re purchasing in Hermosa Beach, where properties often carry coastal easements, utility restrictions, or complex ownership histories, extra buffer time prevents the scenario where a title problem forces you to renegotiate or walk away days before closing.

Reach out to the title company during your initial offer phase, not after your offer is accepted. This early engagement lets you understand what documentation the title company will need and what red flags commonly appear in your specific area.

Review the Preliminary Title Report With Legal Guidance

Request a preliminary title report as soon as your purchase agreement is signed, then review it thoroughly with an attorney who understands California real estate. Don’t assume the preliminary report is complete or final-California Insurance Code section 12414.30(b) explicitly states that preliminary reports are merely offers to issue insurance, not guarantees of title condition. The report tells you what needs fixing, but you need someone with legal knowledge to interpret whether each issue poses real risk to your investment or is a standard exception you can accept.

Many investors skip this step and regret it when they discover post-closing that an easement or restriction they thought was resolved actually affects their development plans or property value. An attorney asks different questions than a title company does: Does this easement block your intended development? Will this restriction prevent future sale to a specific buyer type? Can you refinance if this lien isn’t fully released? These questions matter far more than the title company’s checklist.

Coordinate Directly With the Title Company’s Underwriting Team

Work directly with the title company’s underwriting team, not just through a real estate agent or broker. Agents have incentives to move deals forward quickly, but your interest lies in catching problems early. Ask the title company specifically about liens, easements, deed restrictions, and any non-record matters that might affect your use of the property.

If the property has been foreclosed, transferred multiple times, or sits in an area prone to boundary disputes, mention this upfront so the title company knows to dig deeper. Request ALTA coverage rather than CLTA if you’re making a substantial investment or planning to refinance later. ALTA policies cost roughly 10 to 15 percent more in premiums but cover non-record risks that CLTA excludes. For Hermosa Beach properties where land values command premium prices, this extra protection justifies the cost and prevents situations where a post-closing discovery forces you to absorb unexpected expenses or accept reduced property value.

Engage an Attorney Before You Sign

Hire a real estate attorney before you sign your purchase agreement, and keep that attorney involved throughout underwriting. Your attorney reviews the title commitment before you’re committed to closing, flags exceptions that could affect your plans, and negotiates with the seller to resolve issues before the final walk-through. Many investors try to save money by handling underwriting alone or relying solely on the title company’s recommendations, but the title company’s job is to insure against known defects, not to advise whether those defects align with your investment strategy.

Maintain Complete Documentation Throughout the Process

Keep all documentation organized in a central file-the purchase agreement, preliminary title report, commitment, all lien releases, survey updates, and correspondence with the title company. When closing day arrives and the title company presents final policies for signature, you’ll have everything you need to confirm that every issue identified during underwriting was actually resolved. This documentation also protects you if a title problem emerges after closing; you’ll have a complete record of what was discovered, what was disclosed, and what insurance was purchased to cover remaining risks.

Final Thoughts

Title underwriting in California practice separates investors who protect their wealth from those who discover problems too late. The process works straightforwardly when you understand what happens at each stage: a thorough title search uncovers hidden liens and ownership defects, a preliminary report identifies what needs fixing, and your attorney confirms that every issue is resolved before closing. In Hermosa Beach and throughout Los Angeles County, properties often carry complex ownership histories and coastal easements that demand careful examination.

Title problems exist in nearly every transaction, and the ones that hurt you most are the ones you don’t catch before closing. Unknown liens, boundary disputes, and unreleased mortgages happen regularly in California deals, not as rare edge cases. Title insurance protects you against defects that existed before you bought, but only if you’ve identified and documented them during underwriting-CLTA policies cover public-record defects, while ALTA policies extend protection to non-record risks.

Professional title services address risk before it becomes your problem. Contact Pierview Law to discuss your real estate transaction and confirm that your title underwriting receives the attention your investment deserves.