Mergers and acquisitions tax planning determines whether you keep more money after closing the deal or watch it disappear to unnecessary tax bills.

At Pierview Law, we’ve seen business owners in Hermosa Beach lose hundreds of thousands of dollars because they didn’t plan the tax side of their transaction properly. The good news is that strategic planning before, during, and after your M&A can save you significantly.

Before You Sell: Get Your Tax House in Order

Understand Your Current Tax Position

The difference between a profitable exit and a tax disaster often comes down to what you do before you sign anything. Most business owners in Hermosa Beach focus on valuation and purchase price, then face tax bills that consume 20 to 40 percent of their proceeds. The IRS doesn’t care about your deal timeline-it cares about your tax position, and that position locks in long before closing.

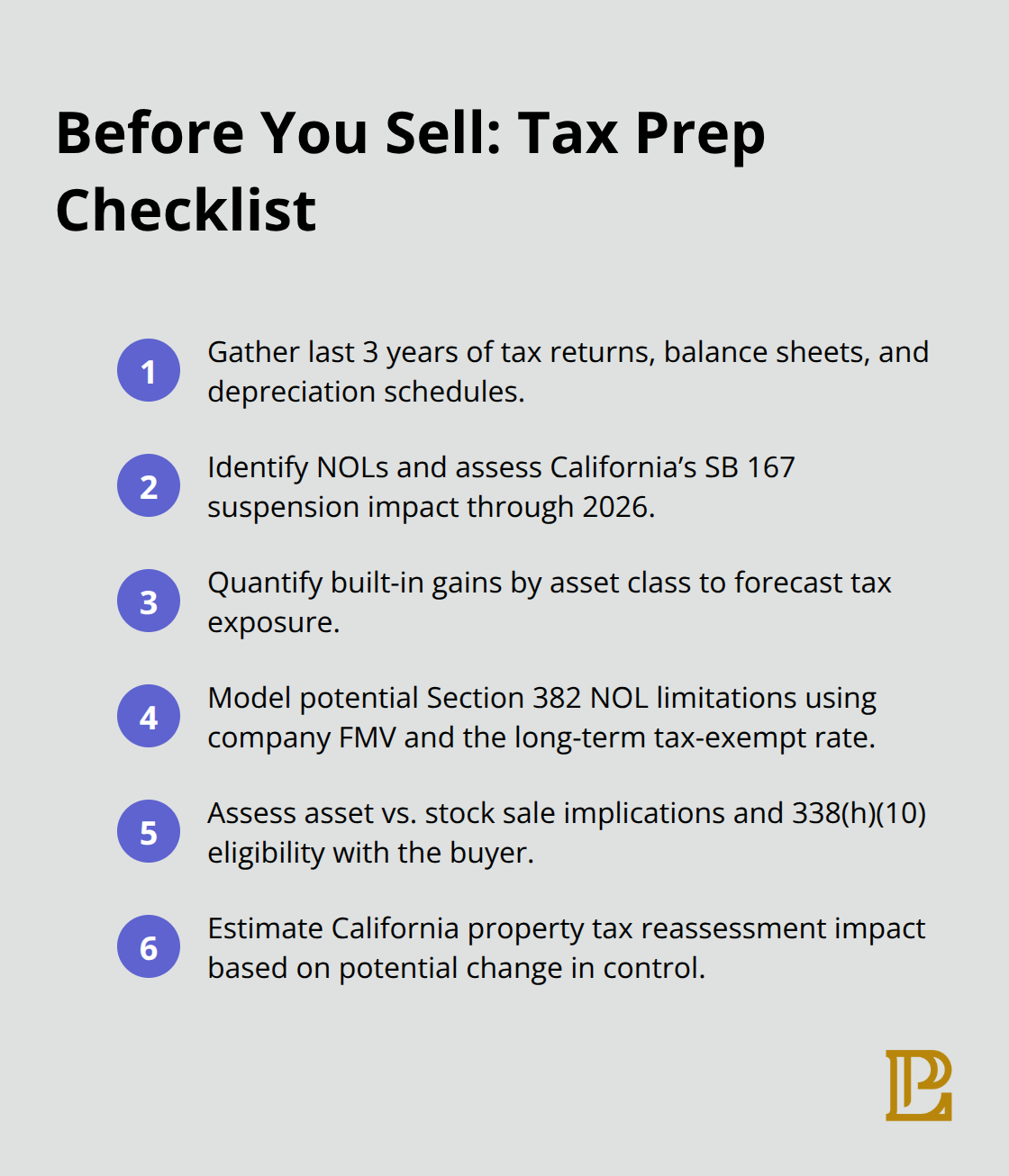

Pull together your last three years of tax returns, balance sheets, and depreciation schedules. Look for net operating losses (NOLs) sitting on your books. If you’re in California, pay close attention: California suspended NOL deductions for 2024 through 2026 under SB 167, which means those losses may be worthless in your state even if they’re valuable federally. This matters because a buyer might structure the deal to use those losses, but if California won’t let them, your negotiating position weakens.

Calculate Your Built-In Gains and Tax Exposure

Calculate your built-in gains and losses across all asset categories. Real property, equipment, inventory, and goodwill each carry different tax consequences when sold. If you’ve held property for years, the gap between your cost basis and current market value is your built-in gain-and that’s what gets taxed at sale.

The Section 382 limitation can severely restrict how much of your NOLs you can use after an ownership change. The limitation is calculated using your company’s fair market value just before the change multiplied by the long-term tax-exempt rate. If your company is worth $5 million and the tax-exempt rate is roughly 2.5 percent, your annual NOL usage might be capped at $125,000, meaning a $2 million loss could take 16 years to use. Understanding this number now lets you price the deal accordingly or structure it differently to preserve value.

Choose the Right Deal Structure

The deal structure you choose-asset sale versus stock sale-determines your entire tax outcome. Asset sales let you step up the basis in assets the buyer acquires, which means higher depreciation and amortization deductions for the buyer going forward, but they’re generally tax-inefficient for sellers because you pay tax on each asset gain separately. Stock sales are cleaner for sellers in most cases because capital gains rates are lower than ordinary income rates, but buyers hate stock deals because they don’t get that basis step-up and they inherit all the company’s hidden liabilities.

A Section 338(h)(10) election can bridge this gap: it lets you treat a stock sale as an asset sale for federal tax purposes, giving the buyer asset-step-up benefits while keeping the stock sale structure. This election requires that the buyer acquire at least 80 percent of your voting power and value, and both you and the buyer must agree to it jointly. The election is powerful, but it’s not automatic-you have to affirmatively make it, and missing the deadline costs you the benefit.

Account for California Property Tax Reassessment

If you’re selling a business with significant real property in California, factor in property tax reassessment. California reassesses real property whenever there’s a change in control of more than 50 percent ownership, which means the county will revalue your property and your property taxes could jump substantially after closing. This reassessment happens on the date control changes, not the closing date, so timing matters.

If you own real estate through your business entity and you’re selling the entity, the property gets reassessed. If you’re selling the real estate separately, the same result occurs. There’s no way around it in most cases, but knowing the number upfront prevents surprises. Contact your county assessor’s office before you negotiate, because this is a real cost that reduces your after-tax proceeds.

Understanding these tax fundamentals positions you to make informed decisions about how to structure your transaction. The next step involves evaluating whether your deal qualifies for tax-free reorganization treatment, which can dramatically change your tax bill and your negotiating leverage.

How Your Deal Structure Shapes Your Tax Bill

Asset Sales Versus Stock Sales: The Tax Difference

The structure you choose during the transaction phase locks in your tax outcome, and changing your mind after signing costs you money or kills the deal entirely. Asset sales and stock sales produce dramatically different tax results, and most business owners in Hermosa Beach don’t understand the gap until it’s too late.

An asset sale means you sell individual assets like equipment, inventory, goodwill, and real property separately. The buyer receives a stepped-up basis in each asset, which generates larger depreciation and amortization deductions for them over time. You pay tax on each asset’s gain individually, which often means ordinary income rates on inventory and depreciation recapture, plus capital gains rates on real property and goodwill.

A stock sale means the buyer acquires your entire company as a going concern, inheriting all assets, contracts, and liabilities in one transaction. You typically pay capital gains tax on your stock proceeds at preferential rates, which sounds better until you realize the buyer receives no basis step-up and refuses to pay full value because they’re stuck with your old, low tax basis in the assets.

Federal Capital Gains Rates and Your After-Tax Proceeds

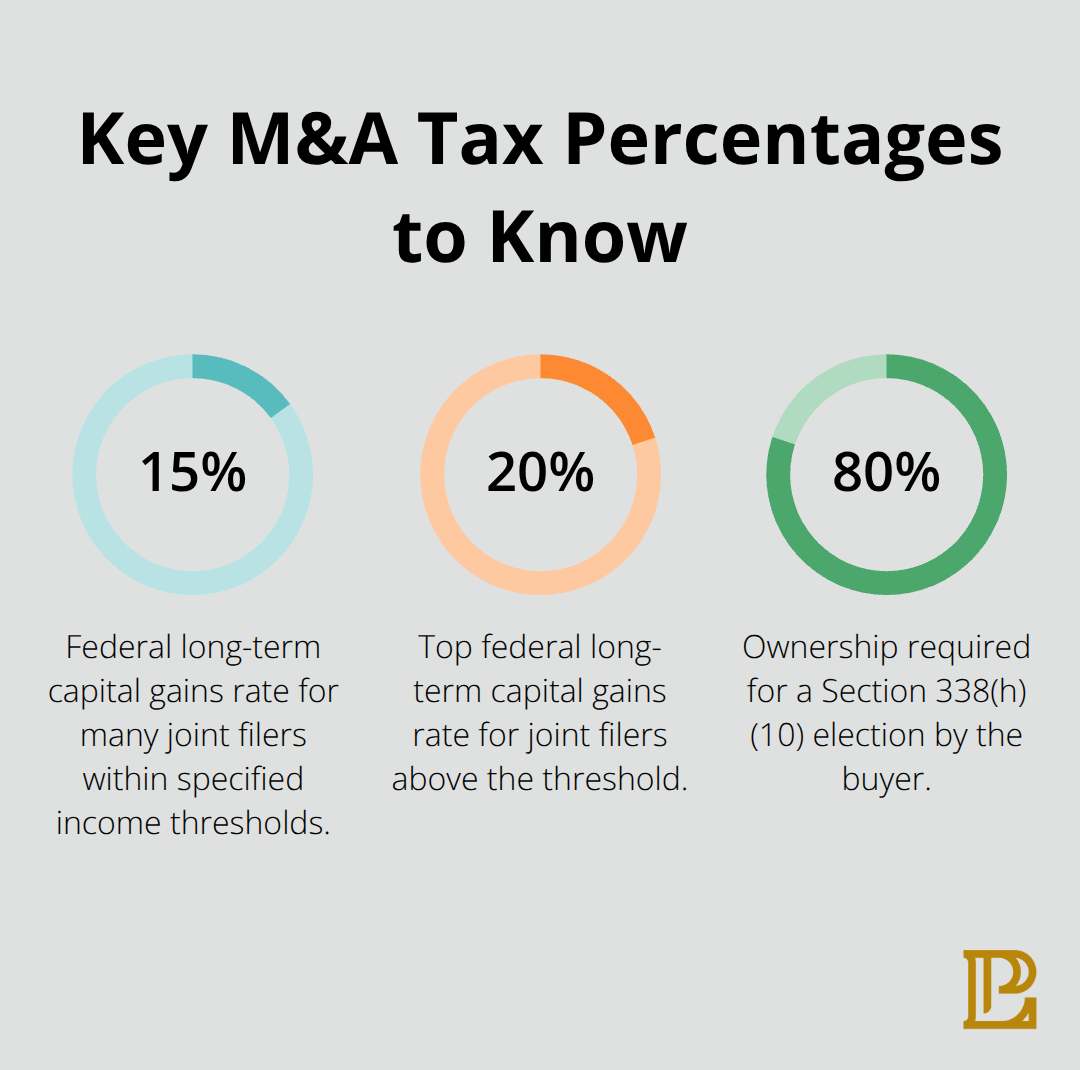

The federal long-term capital gains rate for 2025 is either 0 percent, 15 percent, or 20 percent depending on your income level, according to the Internal Revenue Service. For married couples filing jointly, the 15 percent rate applies to income between $94,375 and $583,750, while the 20 percent rate kicks in above that threshold. This means your stock sale could face taxation at 20 percent while an asset sale would generate a mix of ordinary income and capital gains, potentially costing you more overall.

The Section 338(h)(10) Election: Bridging the Gap

A Section 338(h)(10) election bridges the gap by treating your stock sale as an asset sale for federal tax purposes. The buyer receives the asset step-up they want, you receive the stock sale structure you prefer, and both sides can negotiate a price that reflects the tax benefits. The election requires the buyer to acquire at least 80 percent of your voting power and value, and both parties must jointly elect it within 12 months of closing.

This election is not automatic, which means you must affirmatively file it with the IRS or lose it forever. Many transactions miss this deadline because the parties assume it happens automatically or forget about it during integration chaos.

Net Operating Losses and the Section 382 Limitation

If your company has net operating losses, the Section 382 limitation applies regardless of structure, capping how much NOL the buyer can use annually based on your company’s fair market value and the long-term tax-exempt rate. California’s NOL suspension under SB 167 remains in effect through 2026, so federal losses might be valuable while state losses sit unused, creating a structural problem that no election can fix.

California Property Tax Reassessment and Deal Timing

The timing of when control changes matters because reassessment of California real property occurs on the date control transfers, not the closing date. If you’re selling a business with real property, contact your county assessor before negotiating to get an accurate reassessment estimate. This number is not negotiable with the buyer, but it directly reduces your after-tax proceeds and should influence your asking price.

Structuring the deal correctly requires understanding which assets drive value, how the buyer plans to use those assets, and what tax attributes your company carries. A technology company with valuable intellectual property and a small real estate footprint might benefit from a stock sale to preserve licensing relationships, while a manufacturing business with environmental liabilities and owned real property might be better served by an asset deal that isolates those risks. The next phase of your transaction involves evaluating whether your deal qualifies for tax-free reorganization treatment, which can dramatically change your tax bill and your negotiating leverage.

After Closing: Your Tax Compliance Roadmap

The day after closing, most business owners face a second job: managing the tax obligations their acquisition created. The transaction documents are signed, the money is in the bank, and now you must handle filing requirements, integration challenges, and compliance deadlines that determine whether you actually keep the proceeds you negotiated for. Clients often make expensive mistakes during this phase because they treat post-closing tax work as an afterthought instead of a critical operational priority.

File Required Tax Elections and Forms Within IRS Deadlines

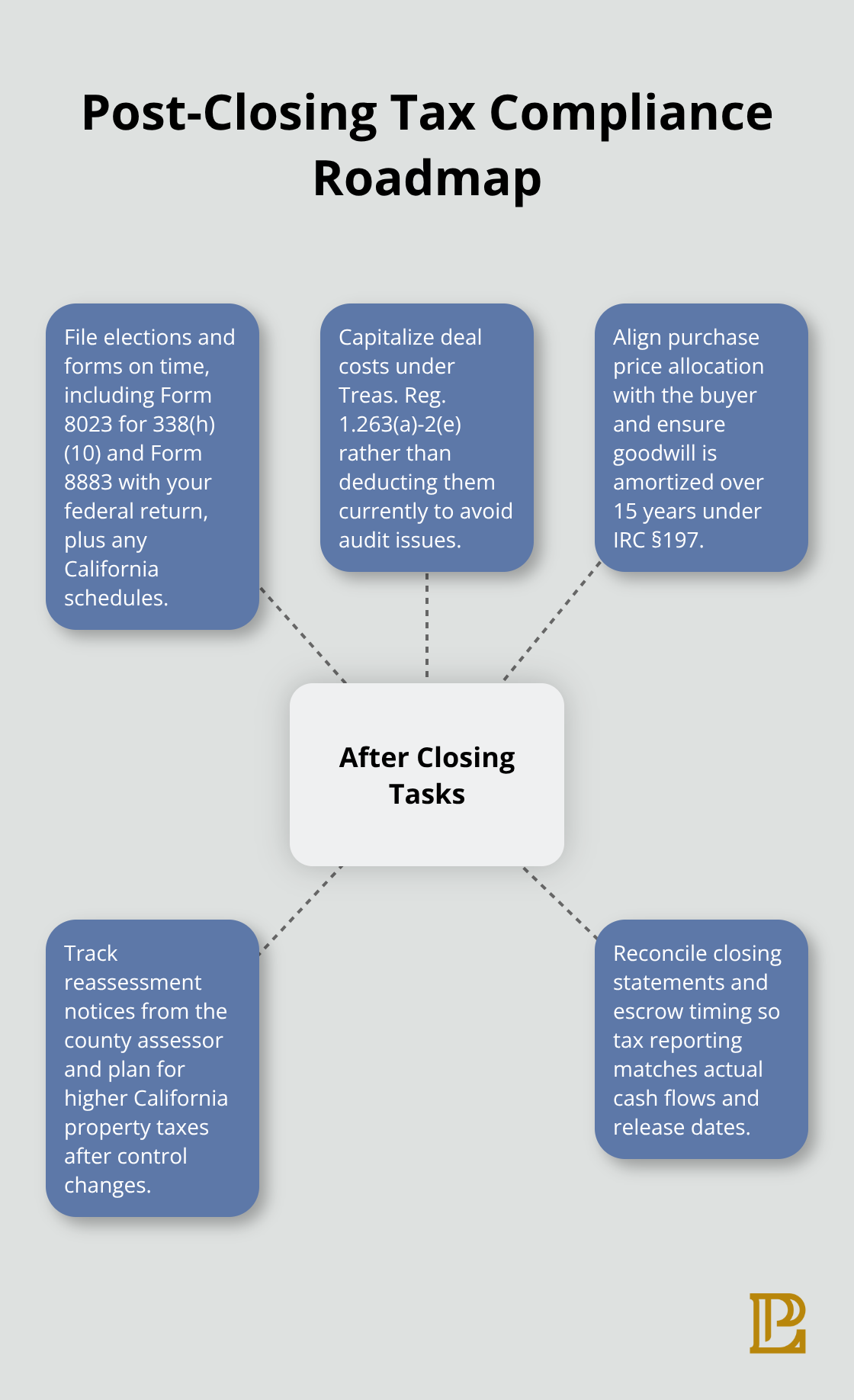

Your first task is to file amended tax returns and entity elections within strict IRS deadlines. If you made a Section 338(h)(10) election, the IRS requires the statement within 12 months of closing, and missing this deadline eliminates the election permanently. File Form 8023 jointly with the buyer and keep a copy in your records. California requires separate reporting of any property tax reassessment changes, and the county assessor will send you a reassessment notice within weeks of closing that triggers a new property tax obligation on the revalued real property. Ignore this notice and you’ll face penalties. If you elected Section 338(h)(10) treatment, you must also file Form 8883 with your federal return to report the deemed asset sale, and California requires Schedule CA to report state-level adjustments.

Capitalize Transaction Costs Correctly

The transaction-related expenses you paid during the deal-including legal, accounting, and broker fees-must be capitalized under Treasury Regulation 1.263(a)-2(e) rather than deducted immediately. This means those expenses reduce your gain calculation rather than generating a current deduction, which changes your tax liability significantly. Document every transaction cost with invoices and categorize them correctly, because the IRS will challenge improper deductions during an audit.

Verify Purchase Price Allocation With the Buyer

Coordinate with your accountant and the buyer’s accountant immediately after closing to verify that purchase price allocation documents are prepared and filed correctly. The IRS requires both parties to report the allocation of purchase price across asset categories consistently, and disagreements between buyer and seller allocations trigger audits. If you sold equipment for $500,000 but reported it as $300,000 while the buyer reported $500,000, the IRS notices the discrepancy and examines both returns. The allocation directly affects depreciation deductions for the buyer and gain calculations for you, so accuracy matters. If your deal involved goodwill, verify that the buyer is amortizing it over 15 years under Internal Revenue Code Section 197, as this confirms the allocation was structured correctly.

Reconcile Closing Statements and Escrow Arrangements

Review your final closing statement against the purchase agreement to confirm all adjustments, prorations, and purchase price adjustments were calculated correctly, because these numbers flow directly into your tax return. If the buyer withheld escrow funds for indemnification obligations, those amounts don’t reduce your gain until the escrow is released or forfeited, which means your tax liability may be higher in the year of closing than you expected. Request a detailed escrow accounting from the buyer’s counsel and understand when funds will be released, because this timing affects your tax planning for subsequent years.

Final Thoughts

Mergers and acquisitions tax planning determines whether you keep your proceeds or watch them disappear to unnecessary tax bills. The three phases we’ve covered-planning before the transaction, structuring during the deal, and managing compliance after closing-form a continuous chain where mistakes in one phase compound into larger problems in the next. Business owners in Hermosa Beach who treat tax planning as a secondary concern behind valuation and purchase price negotiation lose hundreds of thousands of dollars because California property tax reassessment, Section 382 limitations, and improper cost capitalization consume the gains they fought for.

Your accountant and the buyer’s accountant will not automatically coordinate on purchase price allocation and tax elections without your active involvement. You must verify that both parties report the transaction consistently to the IRS, because discrepancies trigger audits that cost you money and time years after closing. Missing IRS deadlines for elections like Section 338(h)(10) treatment eliminates those elections permanently-there are no extensions, no second chances, and no exceptions-and locks you into a less favorable tax outcome.

Contact Pierview Law to discuss your mergers and acquisitions tax strategy and how to structure your transaction for maximum efficiency. We work with business owners throughout Los Angeles County to handle entity formation, contract drafting, and the legal complexities that accompany M&A transactions. Schedule a consultation to review your specific situation, because the tax planning decisions you make now determine your after-tax proceeds for years to come.