Mergers and acquisitions law governs some of the most complex business transactions. Whether you’re buying a company, selling your business, or merging with another firm, the legal details matter enormously.

At Pierview Law, we guide Hermosa Beach business owners through every phase of M&A transactions. This guide walks you through the essential steps to protect your interests.

Understanding Mergers and Acquisitions

What Happens in a Merger Versus an Acquisition

A merger combines two companies into one legal entity, while an acquisition occurs when one company purchases another and typically operates it as a subsidiary or integrates it into existing operations. The distinction matters legally because mergers trigger different filing requirements, shareholder votes, and continuity of obligations than acquisitions do. In a merger, both companies technically cease to exist and form a new entity, meaning creditors, contracts, and liabilities flow automatically to the combined organization. In an acquisition, the buying company assumes only the assets and liabilities it explicitly agrees to take on, giving buyers more control over what they inherit. This difference shapes your entire deal structure, tax treatment, and post-closing exposure. For Hermosa Beach business owners considering either path, understanding which route fits your situation prevents costly mistakes down the line.

The People Who Make M&A Happen

M&A transactions require coordination across multiple roles, and each player affects the deal’s success. The seller and buyer drive the core business terms and strategic goals, but they cannot execute the deal alone. M&A attorneys function as central deal-makers who coordinate corporate, tax, employment, and regulatory matters simultaneously. Accountants and financial advisers handle valuation, tax structuring, and due diligence on earnings quality. Bankers or brokers often facilitate introductions, manage confidentiality, and structure offers in Hermosa Beach and Los Angeles County markets. Employment counsel reviews benefit plans, change-of-control agreements, and retention packages for key staff. Real estate specialists verify title, lease assignments, and landlord consents when property transfers as part of the deal. Insurance brokers ensure tail coverage for directors and officers liability survives closing. When you involve the right professionals early-rather than after problems surface-deal momentum accelerates and hidden liabilities surface before they become your problem.

Five Distinct Phases That Define Your Timeline

The M&A process unfolds across five phases, and timing varies dramatically based on deal complexity. In the Assessment phase, the seller prepares financial records, corporate documents, and an informational memorandum to help buyers decide whether to pursue the opportunity seriously. Negotiations and Letter of Intent follow, where counsel addresses antitrust pre-clearance, employment issues, and fiscal implications while drafting the letter of intent. Due Diligence typically consumes the longest window-often 60 to 90 days-involving comprehensive legal and financial review by both buyer and seller to verify information and identify risks. After due diligence, Negotiation and Closing phases finalize purchase agreements, resolve open questions, and prepare closing documents. Post-Closing Integration, though often overlooked, determines whether the combined entity actually functions as planned and includes governance alignment, IT system consolidation, and cultural integration. Most transactions take four to eight months from initial assessment to closing, though complex deals involving regulatory clearance or multiple jurisdictions can extend to 12 months or longer.

Once you understand which phase you occupy, you can plan resource allocation and manage stakeholder expectations throughout the process. The next chapter examines the legal due diligence and compliance requirements that protect your interests before you commit to the transaction.

Legal Due Diligence and Compliance Requirements

Financial Records Reveal the True Picture

Due diligence is not a box-checking exercise. It is your only opportunity to uncover problems before you are legally bound to the transaction. Most business buyers and sellers approach due diligence reactively, responding to requests from the other side rather than driving a systematic investigation. This approach leaves money on the table and exposes you to liabilities you did not anticipate.

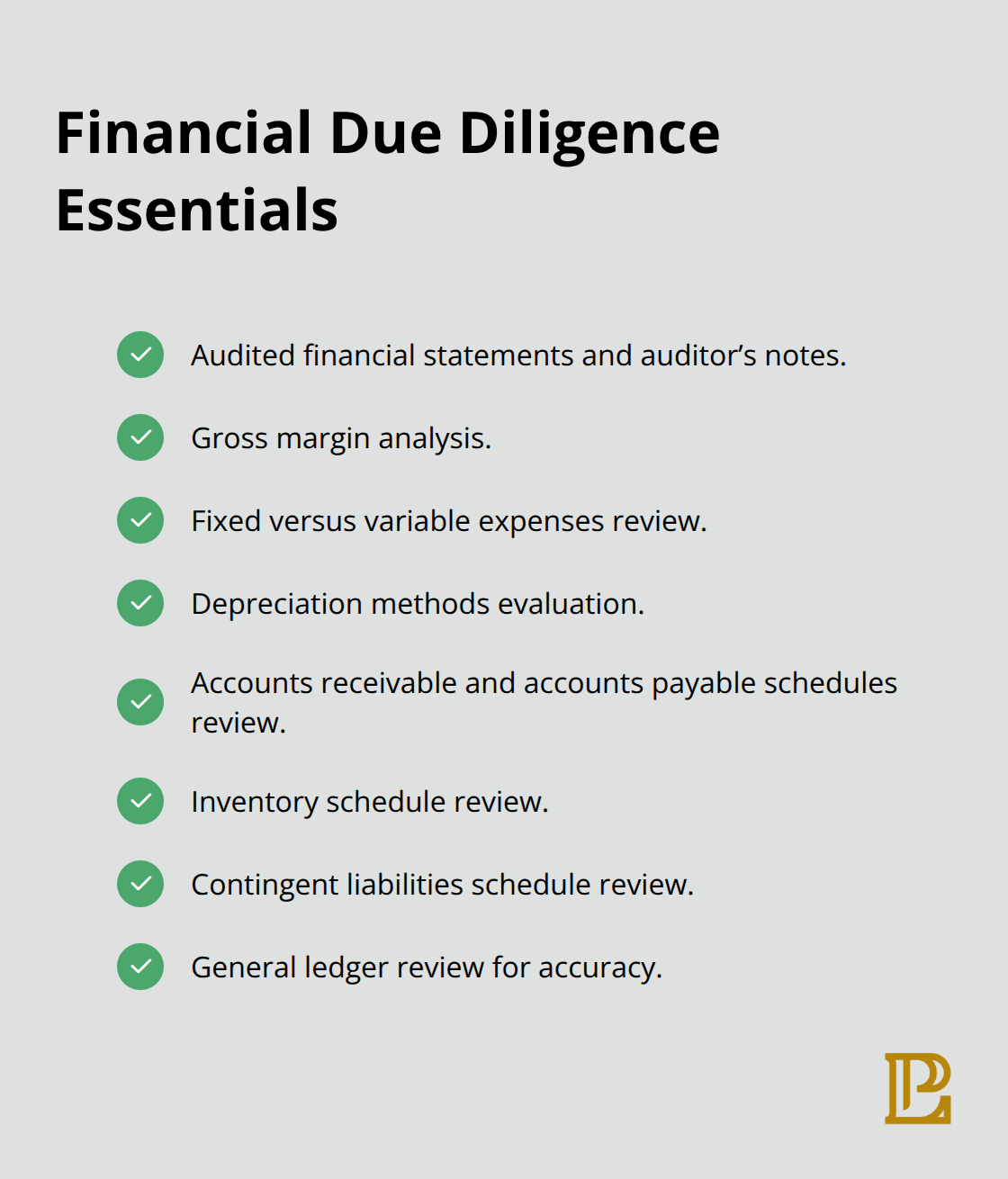

Financial records demand the most scrutiny. Obtain audited financial statements and the auditor’s notes, not just compiled statements, because auditor findings reveal internal control weaknesses and accounting adjustments that affect earnings quality. Analyze gross margins, fixed versus variable expenses, and depreciation methods to understand profitability structure. Request schedules of accounts receivable, accounts payable, inventory, and contingent liabilities to assess true liquidity risk.

A company showing strong revenue growth but deteriorating margins or rising receivables signals operational stress that will transfer to you after closing.

Review the general ledger for consolidation accuracy and potential misstatements. Corporate records including Articles of Incorporation, Bylaws, and minutes confirm ownership structure and governance. Shareholder agreements often contain restrictions on transfers, voting rights, or drag-along provisions that affect your purchase price or timeline. Verify the company’s state registrations and identify every jurisdiction where it operates, owns property, or maintains employees because each location creates separate tax and regulatory exposure.

Customer and Contract Risks Shape Deal Value

Customer concentration represents the single largest risk most buyers overlook. If one customer represents more than 20 percent of revenue, you inherit severe cash flow risk the moment you close. Require written confirmation from major customers that they will continue the relationship post-closing, or build price holdbacks tied to customer retention.

Contracts form the operational backbone of any business, so compile all material agreements and flag change-of-control provisions that may trigger price adjustments, termination rights, or consent requirements. Real estate leases deserve particular attention in Hermosa Beach transactions because landlords often refuse to consent to lease assignments unless the buyer meets specific credit thresholds or pays additional fees. Request estoppel certificates from landlords confirming lease terms, rent amounts, and any defaults. Environmental permits and hazardous substance disclosures are non-negotiable in retail and hospitality sectors, especially for restaurants and food service operations.

Hidden Liabilities Surface Through Systematic Investigation

Start by building a structured due diligence checklist that covers financials, customers, contracts, compliance, HR, litigation, intellectual property, real estate, and taxes. Assign ownership of each category to a specific person and track open questions weekly. Litigation history, employment disputes, and workers compensation claims reveal operational stress and cultural problems that persist after closing.

Tax returns for the past three to five years, combined with any IRS correspondence or tax liens, expose hidden liabilities that survive closing under indemnification provisions. Once due diligence findings surface, use them to drive price adjustments, escrow holdbacks, or earn-out terms rather than accepting issues at face value.

Regulatory Approvals and License Transfers Determine Closing Timeline

Regulatory approvals vary by industry and deal structure. If the transaction involves healthcare, defense contracting, or financial services, federal approval timelines can extend six to twelve months. Antitrust review applies when the combined entity would control significant market share in a defined geographic area, and the Federal Trade Commission scrutinizes deals in concentrated markets with few competitors. In Hermosa Beach and Los Angeles County, retail and hospitality consolidation sometimes triggers local review if market concentration becomes problematic.

License transferability is often the forgotten regulatory hurdle. Beer and wine licenses, full liquor licenses, food service permits, and professional certifications do not automatically transfer to the buyer. Verify transferability with licensing authorities and obtain written confirmation that you will be approved as the new licensee before closing. Franchisor approvals add another layer of delay if the business operates under a franchise agreement. The Franchise Disclosure Document governs transfer rights and royalty obligations, so review it carefully and confirm the franchisor will consent to your ownership.

These approvals should be obtained in parallel with financial due diligence, not sequentially, because regulatory delays are the leading cause of deal extension and increased transaction costs. Once you complete due diligence and secure regulatory clearances, you move into the critical phase where deal structure and negotiation terms determine whether the transaction protects your financial interests or exposes you to unexpected liabilities.

Structuring the Deal and Negotiating Terms

Asset or Equity: Which Structure Protects Your Interests

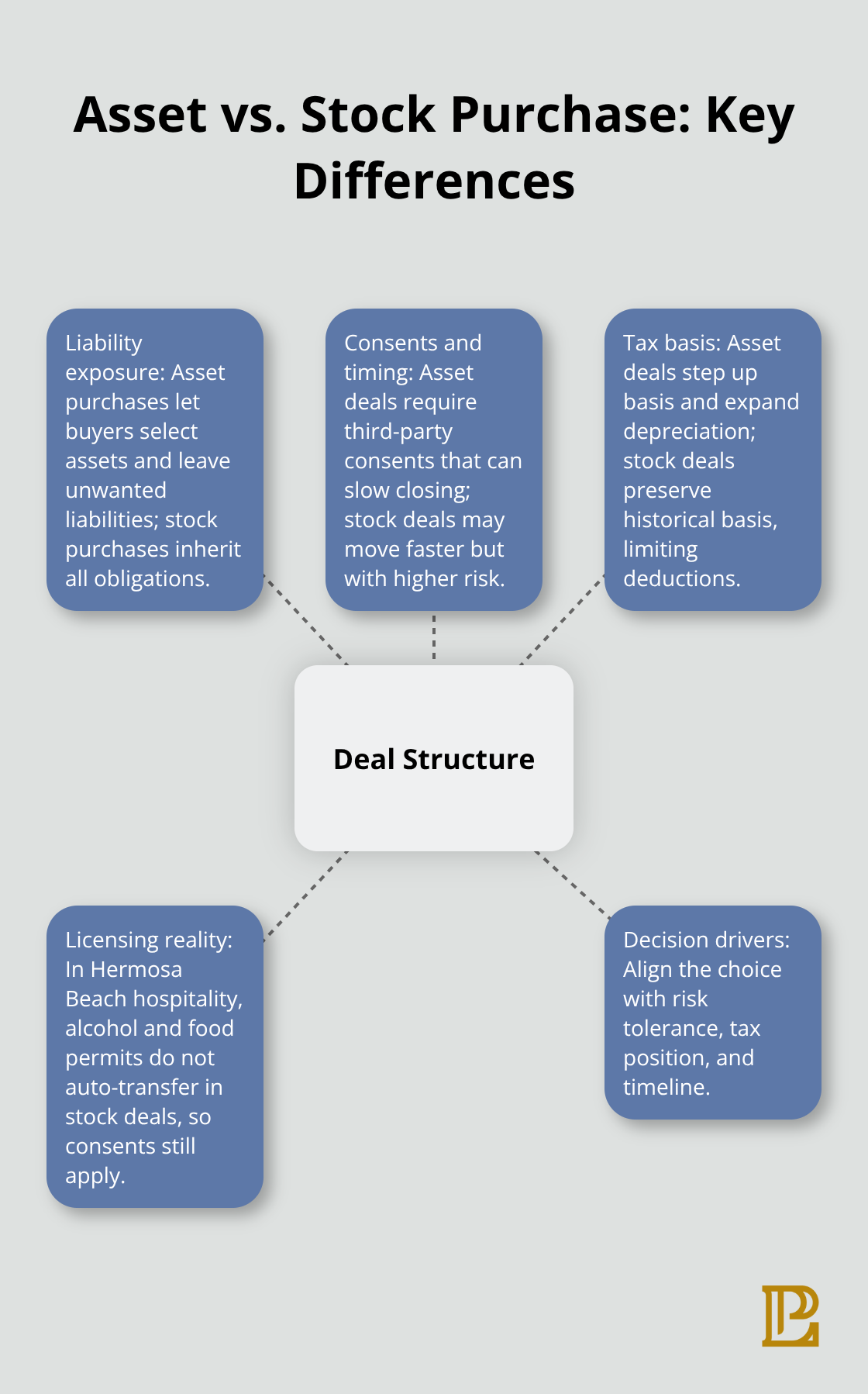

The choice between an asset purchase and a stock purchase fundamentally determines your financial exposure after closing. In an asset purchase, you acquire only the specific assets you want and leave behind liabilities the seller retains. In a stock purchase, you inherit everything, including hidden debts, pending lawsuits, and tax disputes that existed before you took over. Most buyers assume stock purchases happen faster because fewer consents are needed, but this speed comes at a steep price. You absorb all historical liabilities whether you knew about them or not, and indemnification provisions often have short survival periods, leaving you vulnerable once those terms expire. Asset purchases require third-party consents for contracts, real estate leases, and licenses, which slows closing but gives you control over what you actually assume. In Hermosa Beach hospitality transactions, for example, beer and wine licenses and food service permits do not transfer automatically in stock deals, so you face the same consent process anyway while carrying unwanted liabilities. The tax treatment differs significantly between structures. Asset purchases let you step up the cost basis of acquired assets and depreciate them over their remaining useful lives, generating tax deductions that reduce your ongoing tax burden. Stock purchases preserve the seller’s historical basis, limiting your depreciation benefits and potentially triggering built-in gain taxes if you later sell appreciated assets.

Your choice should align with three factors: your risk tolerance, your tax position, and your timeline. If the target company operates in a heavily regulated industry or has complex litigation history, an asset purchase isolates you from those problems. If you need to close quickly and the seller’s liabilities are minimal and well-documented, a stock purchase may make sense. Work with your tax adviser and legal counsel simultaneously to model both structures before negotiations begin, because changing course mid-deal costs time and credibility.

Representations and Warranties Determine Recourse After Closing

Representations and warranties are contractual promises about what is true regarding the business being sold. The seller represents that financial statements are accurate, that no undisclosed litigation exists, that intellectual property is properly owned, and that all material contracts are in full force. These promises are your only recourse if the business is not as represented, and their scope and duration directly affect your post-closing protection. Many buyers accept vague reps or short survival periods because they want to close quickly, then regret that decision when problems surface months later. Specific and detailed reps matter more than lengthy ones. Instead of a generic representation that the business complies with all laws, require the seller to represent specifically that no environmental liens exist, that all workers compensation premiums are current, and that no OSHA violations have been cited in the past three years. The survival period determines how long after closing you can bring indemnification claims. Standard practice is 18 to 24 months for general reps and 3 to 5 years for tax and environmental matters. Shorter periods favor the seller but expose you to discovering problems just after your remedy expires. Escrow holdbacks and earn-out provisions tie a portion of the purchase price to post-closing performance or the absence of claims, effectively extending your protection beyond the survival date. If you agree to an earn-out, specify exactly which metrics you will measure, how frequently you will report results, and what happens if you and the seller disagree on the calculation. Vague earn-out language creates disputes that consume management time and legal fees long after closing.

Contingencies and Closing Conditions Protect Against Deal Failure

Closing conditions are contractual triggers that must be satisfied before either party is obligated to complete the transaction. Common conditions include obtaining regulatory approvals, third-party consents, financing commitments, and the absence of material adverse changes. Too many buyers view closing conditions as formalities and fail to specify what happens if a condition is not met. If you make closing contingent on negotiating favorable terms and the landlord refuses, do you have the right to walk away, renegotiate price, or are you stuck? The agreement must state this explicitly. Material adverse change clauses protect you if the business deteriorates significantly between signing and closing, but courts interpret these narrowly because sellers need closing certainty. A material adverse change must be substantial and unexpected, not a normal cyclical downturn in the industry. If you are buying a restaurant and customer traffic drops 30 percent because of a temporary local construction project, that does not typically qualify as a material adverse change. Define what constitutes a material adverse change upfront, with specific dollar thresholds and exclusions for industry-wide disruptions. Financing contingencies require you to obtain committed funding by a specific date, and most lenders require the seller to warrant that no material changes have occurred since the initial due diligence phase. If the seller cannot provide updated reps or if conditions have genuinely changed, the lender may withdraw the commitment, forcing you to renegotiate or walk away. Build in a 60 to 90 day window for financing approval and regulatory clearance, and require the seller to cooperate in obtaining updated certifications from third parties. The agreement should also specify what happens at closing if a condition cannot be satisfied, including whether parties can waive the condition, extend the deadline, or terminate the deal without penalty.

Final Thoughts

M&A transactions succeed when you protect your interests at every stage, from initial due diligence through post-closing integration. The most common mistake Hermosa Beach business owners make is rushing to close without addressing the details that matter most. You cannot recover from overlooking customer concentration, failing to verify license transferability, or accepting vague representations about liabilities.

At Pierview Law, we guide Hermosa Beach and Los Angeles County business owners through mergers acquisitions law by coordinating every phase of your transaction. We prepare your business for sale, negotiate purchase agreements that protect your interests, and work alongside your tax adviser to model different deal structures. Our team manages post-closing integration planning to align governance, systems, and operations with your strategic goals.

After closing, notify major customers of the ownership change and consolidate IT systems to eliminate redundancy. Verify that insurance tail coverage for directors and officers liability is in place and that all regulatory licenses transfer properly. Contact Pierview Law to discuss your M&A transaction and learn how we structure deals that protect your financial interests while keeping momentum toward closing.