Cross-border M&A in California involves layers of complexity that most business owners underestimate. International transactions demand attention to tax codes, regulatory frameworks, and legal structures that differ dramatically from domestic deals.

At Pierview Law, we’ve guided countless clients through these intricate processes. This guide walks you through the financial, legal, and strategic considerations that determine whether your cross-border acquisition succeeds or stumbles.

What Makes Cross-Border M&A Different from Domestic Deals

Cross-border acquisitions in California operate under fundamentally different rules than domestic transactions. A domestic deal involves one set of tax codes, one regulatory body, and one legal system. International transactions force you to navigate dual tax systems, foreign investment screening, antitrust enforcement across multiple jurisdictions, and compliance frameworks that shift depending on the target’s home country. California’s regulatory environment-including privacy law enforced by the California Privacy Protection Agency and non-compete restrictions-layers onto federal requirements and foreign rules. This directly affects deal timing, cost, and structure. A transaction that might close in 90 days domestically stretches to 180 days or longer when foreign direct investment review, antitrust clearance in another country, and sector-specific permits enter the picture. The California Privacy Protection Agency has demonstrated willingness to impose meaningful penalties, which means cross-border deals involving California assets now require bespoke data security covenants and pre-closing remediation that didn’t exist five years ago.

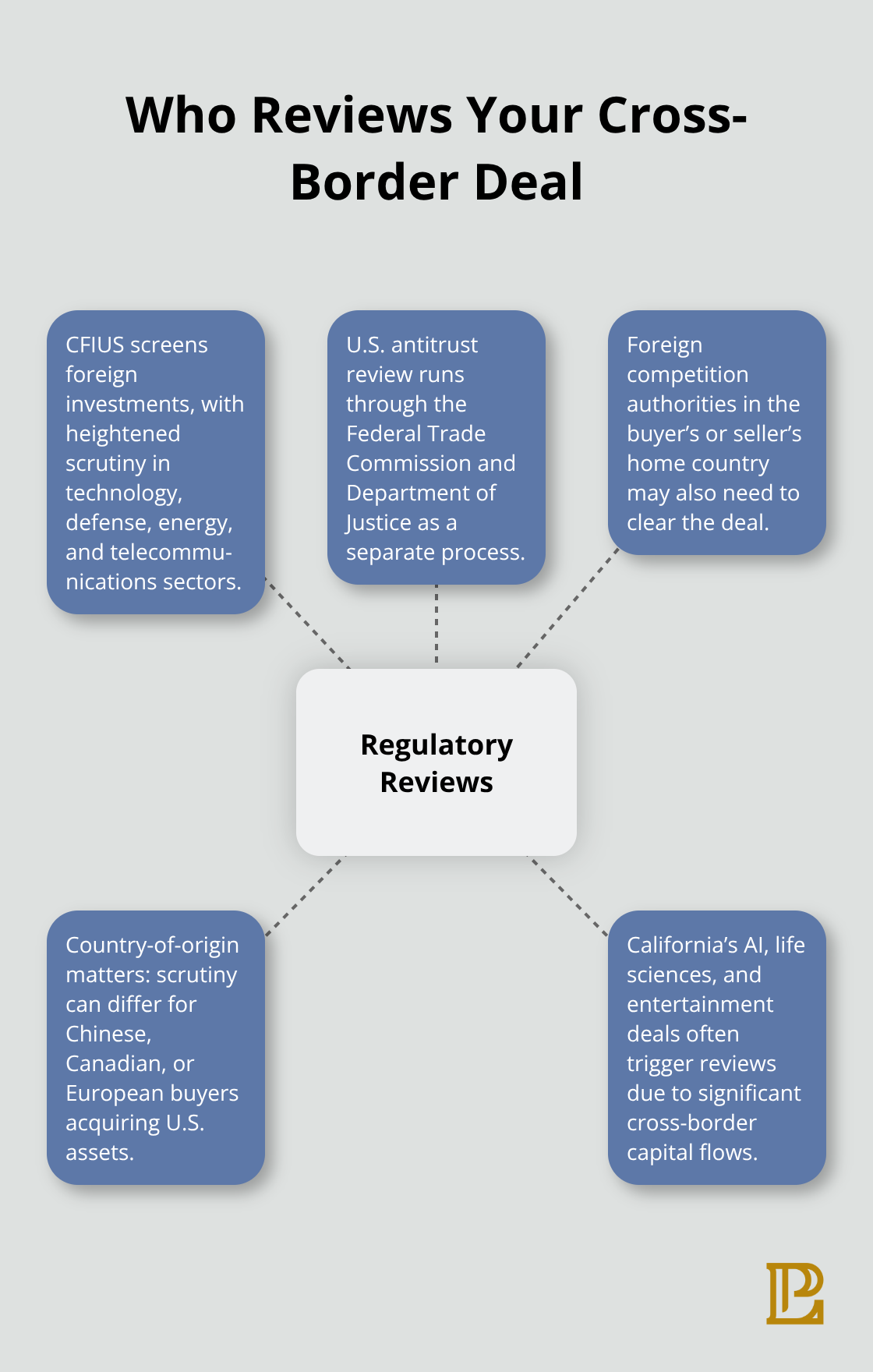

Foreign Investment Screening and Antitrust Review

Foreign investment screening in the U.S. falls under CFIUS (Committee on Foreign Investment in the United States), and certain sectors-technology, defense, energy, telecommunications-face heightened scrutiny. California’s AI, life sciences, and entertainment industries attract significant cross-border capital, which means many deals trigger CFIUS review. The target’s country of origin matters enormously. A Chinese buyer acquiring a U.S. software company faces different scrutiny than a Canadian or European buyer. Antitrust review operates separately; the Federal Trade Commission and Department of Justice enforce U.S. antitrust law, but foreign buyers must also satisfy competition review in their home countries.

A transaction might clear U.S. antitrust review but fail in the EU or China.

Healthcare and Life Sciences Compliance

California life sciences deals face additional complexity under Assembly Bill 1415, which became effective January 2026 and expanded the California Department of Health Care Access and Information’s review of certain healthcare transactions. Private equity and hedge funds acquiring healthcare assets now must provide at least 90 days’ notice before closing, fundamentally altering deal timelines and structuring. This regulatory shift requires you to plan for extended timelines and build remedy frameworks into your transaction structure from the outset.

Intellectual Property Protection Across Borders

Intellectual property considerations demand separate protection strategies per country; patents registered in the U.S. don’t automatically transfer protection to Europe or Asia, requiring country-by-country IP audits and potential re-filing costs. You must treat IP protection as a distinct workstream within your due diligence process, not an afterthought.

Why Cross-Border Buyers Target California Assets

California accounts for roughly one-third of U.S. venture capital activity and hosts the nation’s largest concentration of AI, life sciences, and entertainment companies. Biocom’s California 2025 Life Science Economic Impact Report documented that California-based life sciences companies attracted 63.1 billion dollars in investment in 2024, with corporate M&A representing roughly two-thirds of that total. Large pharmaceutical companies continue acquiring later-stage, de-risked life sciences assets to address pipeline gaps and patent expirations. In AI, seed and early-stage funding rounds frequently exceed 100 million dollars, with large incumbents acquiring smaller AI-native startups to accelerate product development and secure proprietary technology. Entertainment and sports transactions remain California deal-making hubs; the Paramount-Skydance consolidation and rising institutional investment in sports leagues like the NWSL illustrate the market’s scale. Music catalog M&A has surged, with private equity firms and institutions forming platforms to scale acquisitions. For foreign buyers, California’s talent pool, established distribution networks, and proven revenue streams justify premium valuations. Non-compete restrictions under California law, however, influence deal structure; sellers and buyers must design retention plans and sale-of-business exceptions to protect key personnel and know-how post-close. The market remains robust, but heightened regulatory scrutiny means successful cross-border deals demand front-loaded compliance positioning and flexible financing structures that accommodate longer timelines and remedy frameworks. Understanding these market dynamics positions you to structure a transaction that attracts the right buyer while managing regulatory risk-a foundation we’ll build on as we examine the tax and financial considerations that shape your deal’s economics.

How Tax and Currency Issues Shape Your Cross-Border Deal

Cross-border M&A deals live or die on tax efficiency, and most California business owners discover this too late. The U.S. taxes worldwide income for U.S. citizens and residents, while foreign sellers often face capital gains tax in their home country plus U.S. federal tax on transaction proceeds. This double taxation risk demands upfront structuring decisions that affect purchase price, payment timing, and deal velocity.

Understanding Double Taxation and Deal Structure

A Canadian seller acquiring a California software company faces Canadian capital gains tax at roughly 50 percent inclusion rates plus U.S. federal tax, state tax, and potentially California’s top marginal rate of 13.3 percent on gains allocated to California operations. The math forces buyers and sellers to evaluate whether the transaction closes as a stock purchase, asset purchase, or merger structure that minimizes total tax burden across both jurisdictions. Asset purchases typically trigger higher state-level taxes in California but may offer the buyer depreciation benefits that justify a higher price. Stock purchases simplify California tax exposure for the buyer but concentrate tax risk on the seller. Run parallel tax analyses under both structures before negotiations begin, not after the letter of intent is signed.

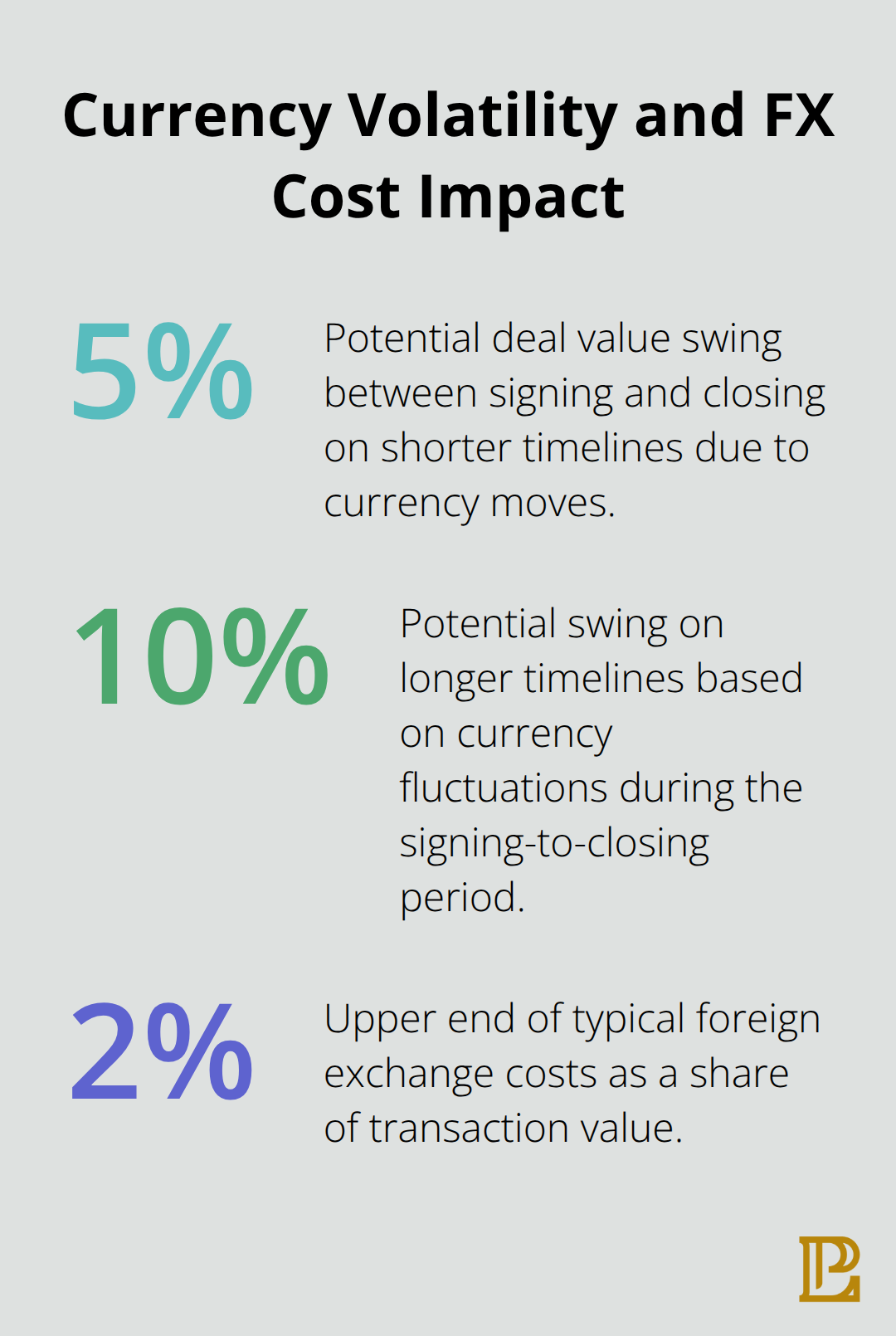

Managing Currency Exchange and Hedging Costs

Currency exchange adds another layer of complexity that accelerates deal costs if not managed early. A Chinese buyer paying in yuan faces exposure to currency fluctuations between signing and closing, which can swing deal value by 5 to 10 percent depending on timeline length. Forward contracts, cross-currency swaps, and multi-currency escrow accounts lock in exchange rates and protect both parties, but they require setup 60 to 90 days before anticipated closing. Waiting until the final week to address currency hedging creates unnecessary risk and often forces unfavorable terms.

Foreign exchange costs typically run 0.5 to 2 percent of transaction value, so a 100 million dollar deal might cost 500,000 to 2 million dollars in hedging expenses alone.

Conducting Rigorous Financial Due Diligence

Financial due diligence in cross-border transactions demands deeper scrutiny than domestic deals because foreign financial reporting standards, hidden liabilities in foreign jurisdictions, and undisclosed regulatory exposure are far more common. The target’s financial statements may comply with International Financial Reporting Standards (IFRS) rather than U.S. Generally Accepted Accounting Principles (GAAP), requiring restatement to align with U.S. buyer expectations and loan covenants. Accounts receivable aging, inventory valuation, and contingent liabilities often hide material exposure that emerges only after forensic accounting review. A European life sciences company may carry environmental remediation liabilities tied to manufacturing facilities that don’t appear on the balance sheet until regulatory action occurs. Engage a Big Four accounting firm early to conduct parallel financial audits under both GAAP and the target’s home country standards, then reconcile the differences. This process typically costs 150,000 to 400,000 dollars but prevents post-close surprises that cost multiples of that amount.

Verifying Revenue Quality and Customer Relationships

Revenue quality matters intensely; cross-border buyers must verify that top-line growth reflects sustainable customer relationships, not one-time contracts or government subsidies that terminate post-close. Conduct detailed customer concentration analysis, contract review, and revenue recognition testing to substantiate growth claims. For California life sciences deals subject to Assembly Bill 1415’s 90-day notice requirement, financial due diligence timelines compress further, making early engagement with financial advisors non-negotiable.

Securing Tax Opinions Across Jurisdictions

Tax opinions from counsel in both jurisdictions address transfer pricing (how intercompany transactions are priced to satisfy both countries’ tax authorities), permanent establishment risk (whether the buyer’s presence in the foreign jurisdiction triggers unexpected tax obligations), and withholding tax on dividends and royalties post-close. These opinions cost 50,000 to 150,000 dollars per jurisdiction but provide legal protection if tax authorities later challenge deal structure. With financial and tax frameworks in place, you shift focus to the legal documentation and negotiation strategy that protects your interests across borders.

Legal Documentation and Negotiation Strategy

Cross-border purchase agreements demand precision that domestic deals rarely require. A California software company acquiring a target in the UK must address which country’s law governs the agreement, how disputes escalate, what happens if tax authorities challenge the deal structure, and whether indemnification survives across time zones and legal systems. Most business owners assume a standard purchase agreement template works everywhere; it doesn’t.

Drafting Purchase Agreements for Multiple Jurisdictions

The agreement must specify payment mechanics in multiple currencies, withholding tax obligations, and escrow arrangements that satisfy both U.S. and foreign tax authorities. If you’re acquiring a life sciences company subject to Assembly Bill 1415’s 90-day notice requirement, the purchase agreement must explicitly address the OHCA approval timeline and build contingencies if regulatory clearance delays closing. Include detailed representations about financial accuracy under both GAAP and the target’s home country accounting standards to prevent post-close disputes over what the seller actually disclosed.

Currency hedging costs should be allocated clearly; decide whether the buyer absorbs FX risk, the seller bears it, or you establish a collar that splits exposure. A 100 million dollar cross-border deal with unfavorable currency allocation can cost an additional 500,000 to 2 million dollars in hidden hedging expenses if not addressed upfront.

Protecting Intellectual Property Across Borders

Intellectual property warranties deserve separate sections; the seller must represent that patents are valid in each jurisdiction where they claim protection, that open-source code compliance has been verified, and that no third-party claims exist. For AI deals, which now trigger intense diligence on data provenance and model training practices according to current California market dynamics, add specific IP reps about data source legitimacy and training methodology. These representations protect you from acquiring hidden IP liabilities that emerge months or years after closing.

Establishing Dispute Resolution Frameworks

Dispute resolution frameworks must account for practical realities of enforcing judgments across borders. Arbitration under the International Chamber of Commerce Rules provides faster resolution than litigation in two separate court systems, but arbitration costs 500,000 to 2 million dollars depending on complexity and can take two to three years. Litigation in California state court or federal court gives you home advantage but makes enforcement of any judgment against a foreign defendant extremely difficult and expensive.

Many sophisticated cross-border deals use tiered dispute resolution: negotiation for 60 days, mediation for 90 days, then binding arbitration in a neutral jurisdiction like New York or London. Specify which country’s substantive law governs the agreement; most California buyers prefer California law because they understand it, but foreign sellers often push for their home country law or English common law as neutral ground. A compromise structure applies California law to commercial terms (price, payment, closing conditions) and English law to dispute resolution mechanics.

Allocating Risk Through Indemnification Terms

Include indemnification baskets and caps that reflect realistic exposure; a 50 million dollar acquisition with a 1 million dollar indemnification basket catches nothing meaningful, while a 5 million dollar basket creates real incentive for the seller to stand behind representations. Time-limit representations carefully: tax matters typically survive three to five years because tax authorities can audit retroactively, while general commercial reps often expire 18 to 24 months post-close. These mechanisms protect your investment and hold the seller accountable for material misstatements that surface after you own the company.

Final Thoughts

Cross-border M&A in California succeeds when you address regulatory complexity, tax exposure, and legal documentation before you sign a letter of intent. The transactions that stumble typically fail because business owners treat these elements as secondary concerns rather than foundational requirements. Start by mapping your target’s regulatory footprint across both jurisdictions, then layer in tax structuring that minimizes double taxation and currency risk.

Common pitfalls emerge when timelines compress. Many buyers underestimate how long foreign investment screening takes or fail to account for Assembly Bill 1415’s 90-day notice requirement for healthcare transactions. Currency hedging gets ignored until the final week, forcing expensive last-minute arrangements, while intellectual property protection receives insufficient attention, leaving you exposed to hidden claims that surface months after closing.

We at Pierview Law guide California business owners through cross-border M&A complexities with practical, business-oriented solutions tailored to your specific transaction. Whether you’re acquiring a foreign target or selling California assets to an international buyer, our team handles entity formation, contract drafting, and the civil litigation support that protects your interests across borders. Contact us to discuss your cross-border M&A strategy and ensure your transaction closes efficiently while managing regulatory risk.