Mergers and acquisitions in California involve complex agreements that can make or break a deal. The difference between a favorable outcome and a costly mistake often comes down to understanding the specific terms and negotiation strategies that matter most.

At Pierview Law, we help business owners navigate California M&A agreements with clarity and confidence. This guide walks you through the essential terms, proven negotiation tactics, and state-specific legal requirements you need to know.

Payment Terms and Risk Allocation in California M&A Deals

How Purchase Price Gets Structured

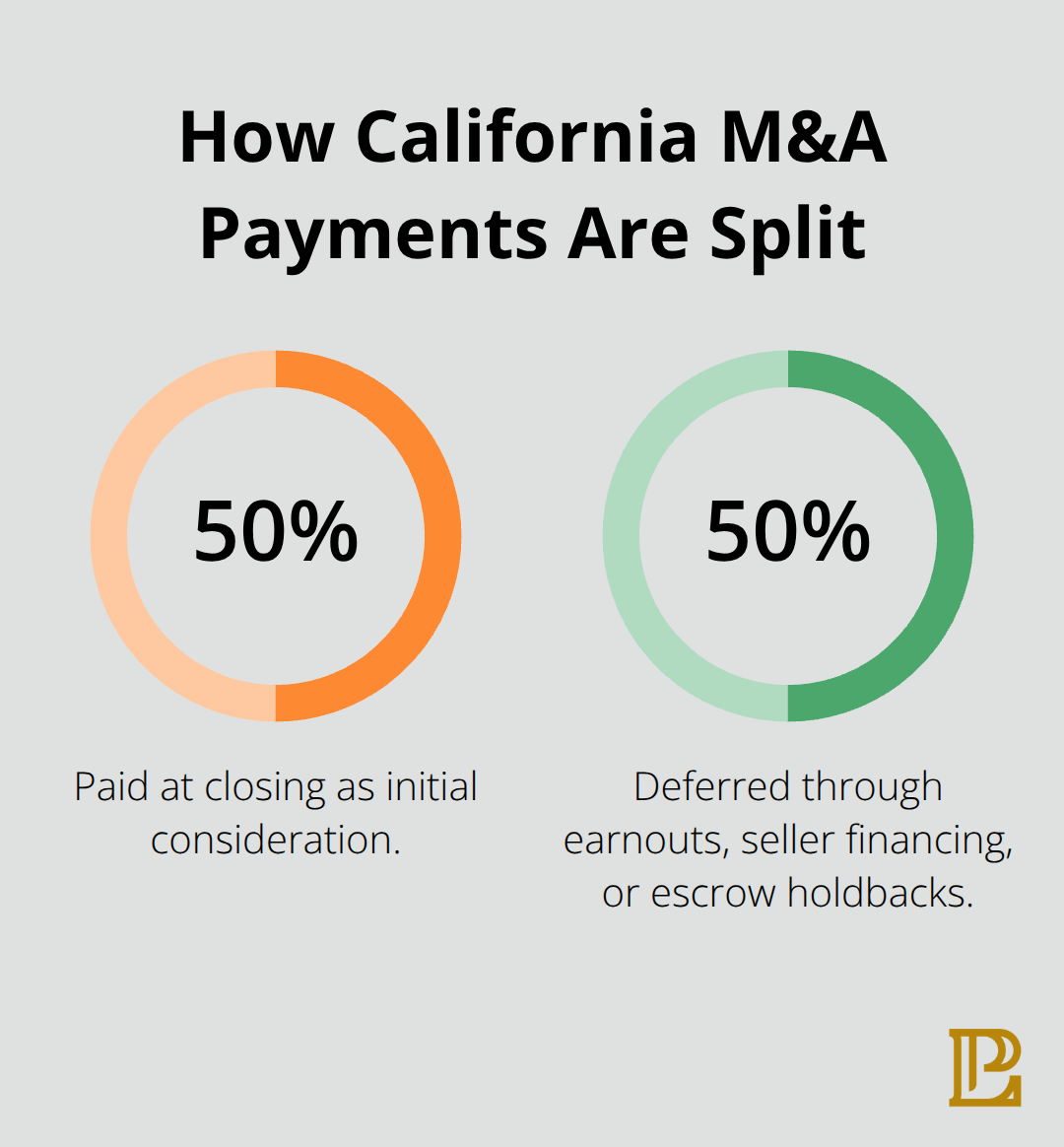

The purchase price in a California M&A deal rarely arrives as a single wire transfer at closing. In Hermosa Beach and across Los Angeles County, most transactions split the payment into roughly 50 percent at closing and 50 percent deferred through earnouts, seller financing, or escrow holdbacks.

For deals under $10 million, seller financing appears frequently, with buyers typically providing 20 to 30 percent of the purchase price via promissory notes payable over 5 to 7 years. This structure protects the buyer by reducing upfront capital requirements and protects the seller by ensuring the buyer maintains genuine skin in the game during integration.

Private equity buyers in the technology sector currently pay premium valuations in the 8 to 12 times revenue range for profitable ventures. Overall deal multiples have compressed roughly 15 percent since early 2024, reflecting tighter valuation conditions. Valuation disagreements have derailed roughly 38 percent of Hermosa Beach M&A deals, with price expectation gaps typically ranging from 25 to 40 percent. Getting the payment structure right from the start prevents costly renegotiations later.

Earnouts and Founder Retention

The earnout component typically requires key founders or sellers to remain employed for 12 to 24 months to receive a substantial portion of the purchase price. Many agreements include acceleration clauses if the buyer terminates employment without cause. This approach ties seller compensation directly to post-closing performance and retention, aligning incentives between both parties during the critical integration window.

Escrow or holdback arrangements usually tie up 10 to 20 percent of the purchase price for 12 to 24 months to cover undisclosed liabilities and other post-closing risks. These funds sit in a neutral account until the survival period expires or claims get resolved.

Representations, Warranties, and Indemnification

Representations and warranties form the foundation of risk allocation in any M&A agreement. The seller represents that financial statements are accurate, contracts are enforceable, no undisclosed liabilities exist, and all necessary licenses and permits are in place. The buyer relies on these statements to make an informed decision, and if they prove false, indemnification provisions determine who bears the cost.

Indemnification requires the seller to defend and pay for pre-closing losses for 12 to 36 months after closing, with the buyer able to claw back funds from escrow or earnout payments when issues surface. Caps on indemnification typically range from 10 to 20 percent of the purchase price, with baskets (minimum thresholds before any claim applies) set between $25,000 and $100,000 depending on deal size. These numbers define your real financial exposure once the deal closes.

A seller who agrees to a 36-month survival period with a 20 percent cap faces far greater post-closing risk than one with an 18-month period and a 10 percent cap. Survival periods should align with your risk tolerance and the complexity of the business being sold or acquired. In California deals, the surviving period for tax-related representations often extends longer than operational ones because tax audits can take years to complete.

Structuring Terms to Match Your Risk Profile

The specific terms you negotiate-survival periods, indemnification caps, baskets, and earnout conditions-directly impact your financial security after closing. Misaligned terms leave you exposed to unexpected liabilities or disputes that drain resources long after the transaction completes. The next section explores how to leverage due diligence findings and negotiation tactics to structure these terms in your favor, whether you’re buying or selling.

Leveraging Due Diligence and Escrow to Shift Negotiating Power

Using Due Diligence Findings as Strategic Leverage

Due diligence findings give you concrete leverage in M&A negotiations, yet most buyers treat findings as a checklist rather than a negotiation tool. When your team uncovers undisclosed liabilities, contract gaps, or compliance issues, you hold information the other side wants to resolve quickly. The Federal Trade Commission reports that preliminary antitrust reviews for deals above $50 million now average around 120 days-delays that cost real money. Present findings methodically to the seller, starting with the most material issues first, and propose specific remedies rather than vague price reductions. A buyer who discovers that a key customer contract contains a change-of-control clause requiring renegotiation should ask the seller to secure written consent before closing, not request a $200,000 price cut and hope for the best. This approach forces the seller to actually solve the problem rather than pass the risk to you.

Structuring Escrow Agreements That Actually Protect You

Escrow accounts function as your financial guarantee after closing, and the structure you negotiate determines whether you can actually recover losses. Most Hermosa Beach deals hold 15 to 20 percent of purchase price in escrow, but the real power lies in the escrow agreement language. Specify exactly which types of claims trigger escrow releases, set clear timelines for claim submission, and define the process for dispute resolution. If your escrow agreement allows the seller to block legitimate claims through procedural objections, you have escrow in name only. We at Pierview Law draft escrow provisions that clearly separate operational claims from tax-related ones, because tax audits often continue well beyond your standard indemnification period.

Matching Indemnification Terms to Actual Risk

Set your indemnification baskets and caps based on actual deal risk, not industry norms. A $5 million technology acquisition with clean financial records and long-term contracts needs far different protection than a $5 million service business with month-to-month client relationships and thin margins. The service business warrants a lower basket (easier to trigger claims), a higher cap, and a longer survival period. A seller who agrees to a 36-month survival period with a 20 percent cap faces far greater post-closing risk than one with an 18-month period and a 10 percent cap. Survival periods should align with your risk tolerance and the complexity of the business being sold or acquired.

Protecting Yourself Through Earnout Structures

Earnout structures create ongoing negotiation long after closing, and vague language here costs sellers real money. If your earnout hinges on revenue targets that depend on sales efforts the buyer controls, you have handed the buyer leverage to reduce your final payout. Protect yourself by defining earnout metrics independently, requiring audited financial statements, and including acceleration provisions if the buyer materially changes operations or terminates you without cause. The typical 12 to 24 month retention period for founders works only if the agreement specifies what happens if the acquiring company restructures your role or eliminates your department. Sellers often accept vague language here and regret it when the buyer reshuffles management six months in.

Planning for Post-Closing Disputes

The specific terms you negotiate-survival periods, indemnification caps, baskets, and earnout conditions-directly impact your financial security after closing. Misaligned terms leave you exposed to unexpected liabilities or disputes that drain resources long after the transaction completes. California deals often extend the surviving period for tax-related representations longer than operational ones because tax audits can take years to complete. These structural choices matter far more than the headline purchase price, and they determine whether integration proceeds smoothly or devolves into claims and counterclaims that consume management attention and legal fees.

California Laws You Cannot Ignore in M&A Deals

Merger Filings and Deal Structure Choices

California imposes specific legal requirements that many out-of-state buyers overlook, and missing these obligations can derail closing or create post-closing liability. The California Corporations Code Chapter 11 mandates that merger transactions file a Certificate of Merger with the Secretary of State, a procedural step that requires coordination with corporate filings, tax registration, and creditor notifications. If you structure your deal as a stock purchase instead of a merger, you avoid this filing requirement, but you assume all pre-closing liabilities the seller accumulated. The choice between asset purchases, stock purchases, and mergers directly determines your regulatory obligations and tax consequences.

Asset purchases let you sidestep seller liabilities but trigger capital gains taxes for the seller, making them resistant to this structure. Stock purchases transfer liabilities to you but appeal to founders and investors because they avoid double taxation. In California deals, stock purchases dominate because founders prioritize tax efficiency over buyer protection, which means you need stronger indemnification provisions to offset the liability exposure you inherit.

Employment Law Compliance and Worker Classification

Employment law creates real friction in California M&A transactions because the state enforces strict wage and hour rules, meal and rest break requirements, and classification standards that many smaller businesses ignore. The California WARN Act requires 60 days notice before layoffs affecting 50 or more employees, and M&A deals frequently trigger restructuring that violates this requirement without careful planning. Many buyers discover post-closing that the seller misclassified workers as independent contractors when California labor standards demand W-2 employment status.

Reclassifying workers after closing costs thousands in back wages, penalties, and payroll taxes that your indemnification basket may not cover. Before closing, hire a California employment attorney to audit the seller’s payroll records, classification decisions, and benefit plan compliance. This audit costs $3,000 to $5,000 but prevents $50,000 to $100,000 in liabilities that surface months after closing.

Environmental and Coastal Compliance Requirements

Environmental compliance matters significantly in Hermosa Beach because coastal properties face tsunami insurance requirements and erosion liability that inland buyers never encounter. If you acquire a business with real estate holdings, your purchase agreement must address environmental assessments, title searches, and coastal zone compliance. These requirements add time and cost to your transaction timeline but protect you from inheriting environmental liabilities that persist for years.

Federal Antitrust Review and Franchise Disclosure

The Federal Trade Commission increasingly scrutinizes horizontal mergers in 2025, with preliminary reviews for deals above $50 million averaging around 120 days. If your M&A transaction combines competitors or creates market concentration concerns, file for FTC clearance proactively rather than hoping regulators overlook the deal. Delays in antitrust clearance can push closing dates back months, disrupting integration plans and management continuity.

California also imposes franchise disclosure requirements that apply if the target business operates franchise relationships or licensing arrangements. These requirements demand detailed financial disclosures and relationship documentation that take weeks to compile. Build 30 to 45 days into your timeline for franchise compliance verification if the target operates through franchisees or licensed partners.

Final Thoughts

California M&A agreements succeed when you treat negotiation as collaborative problem-solving rather than zero-sum combat. The terms you finalize-purchase price structure, indemnification caps, survival periods, and earnout conditions-determine whether your deal creates value or generates disputes that drain resources for years. Most transactions fail not because the headline price was wrong, but because the underlying agreement left critical gaps that surface during integration.

The most common pitfall we see is underestimating California-specific legal requirements. Buyers from out of state often overlook employment law compliance, environmental assessments, and franchise disclosure obligations until closing approaches, forcing expensive delays or post-closing liability. Sellers frequently accept vague earnout language and regret it when the buyer reshuffles operations and reduces their final payout. Both parties sometimes treat indemnification baskets and caps as boilerplate when these numbers directly determine your actual financial exposure after closing.

We at Pierview Law help business owners and buyers structure California M&A agreements that actually protect their interests while keeping deals moving toward closing. Our team handles entity formation, contract drafting, and the full range of business law services needed to support your transaction from initial assessment through post-closing integration. Reach out to discuss your M&A transaction and ensure your agreement reflects your actual risk tolerance and strategic objectives.