Starting a business in Hermosa Beach requires more than just a good idea. You need the right legal structure, proper documentation, and a clear understanding of what comes next.

At Pierview Law, we’ve guided countless founders through Hermosa Beach startup formation. This guide walks you through the decisions and steps that actually matter when launching your business.

Which Business Structure Fits Your Hermosa Beach Startup

The structure you choose determines how much personal liability you face, how much you pay in taxes, and how much flexibility you have as your business grows. Most Hermosa Beach founders narrow it down to three options: sole proprietorship, LLC, or corporation. Each has real tradeoffs that affect your bottom line and your personal assets.

Sole Proprietorship: Simplicity Without Protection

A sole proprietorship is the fastest way to start. You own the business outright, profits flow directly to your personal tax return, and you file no state formation documents. If you operate under a name other than your own, you file a Fictitious Business Name Statement with the county, and you’re essentially done. The California Secretary of State has no involvement. This structure works if you have minimal liability risk and want zero administrative overhead. The problem is personal liability. If a client sues your business or your business incurs debt, creditors can come after your personal bank account, your home, and your other assets. About 90 percent of California startups fail, and legal missteps are a major but often overlooked cause.

A sole proprietorship leaves you exposed to that risk without any buffer. For service-based businesses with low risk, it might work. For anything else, it’s a gamble.

LLC: The Practical Choice for Most Founders

An LLC shields your personal assets from business liabilities. If someone sues your business, they can’t touch your personal savings or home. That protection alone is worth the modest filing fee and ongoing paperwork. A California LLC requires you to file Articles of Organization through the Secretary of State’s online system, plus an internal operating agreement that stays in your records. You avoid the double taxation that corporations face. An LLC taxed as a sole proprietor or partnership avoids the corporate-level tax hit that shareholders pay again on dividends. Most Hermosa Beach startups choose an LLC because it offers liability protection, simpler tax treatment, and more flexibility in how you allocate profits among owners. The California Franchise Tax Board and the Secretary of State both provide resources on formation details.

Corporation: When You Plan to Raise Capital

A corporation requires you to file Articles of Incorporation and makes sense if you plan to raise venture capital or issue stock. Investors expect a corporate structure. A corporation is taxed at the corporate level and again at the shareholder level, which often means double taxation. That tax burden matters less when you reinvest profits back into growth rather than taking them out as personal income. For bootstrapped founders without outside investors, a corporation typically costs more in taxes and administrative work than an LLC. The choice between these structures affects your funding options, tax bill, and how much control you retain as the business scales. Selecting the right entity based on your specific tax situation, ownership plans, and growth timeline prevents costly mistakes later.

How to File Your Business Formation Documents in Hermosa Beach

Register Your Business Name First

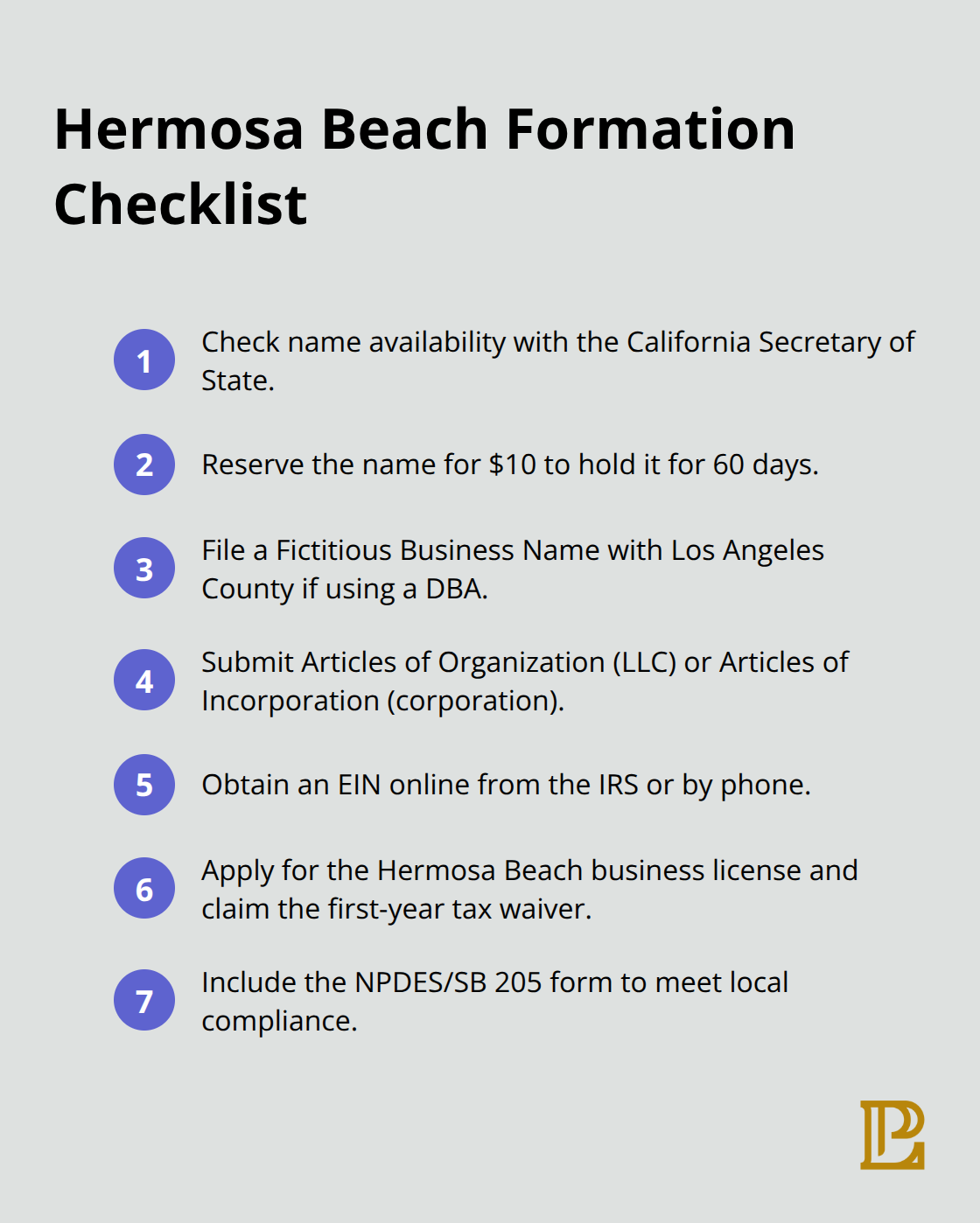

Your business name must be unique in California. Check availability on the Secretary of State’s website before filing anything. If you want to reserve the name while you prepare your formation documents, file a Name Reservation for just $10.

That holds the name for 60 days. Once your state filing is approved, file a Fictitious Business Name Statement with the Los Angeles County Clerk if your Hermosa Beach business operates under a name different from your own. That filing costs roughly $30 to $50 and publishes your business name locally.

File Your Articles of Organization or Incorporation

For an LLC, you file Articles of Organization through the California Secretary of State’s online system at bizfileOnline.sos.ca.gov. Select Register a Business under the Business Entities tile, then complete the Articles of Organization form for a California LLC. For a corporation, you file Articles of Incorporation through the same portal with comparable fees. The filing fee runs about $70 to $100 depending on your specific situation. The Secretary of State processes most filings within two to three business days.

Obtain Your Employer Identification Number

Secure an Employer Identification Number from the IRS while you wait for your state filing to process. You apply online at IRS.gov or by phone at 800-829-4933. The IRS issues your EIN immediately if you apply online. You don’t need an EIN if you’re a sole proprietor with no employees, but most LLCs and corporations should get one anyway since it separates your business finances from personal ones and makes tax filing cleaner.

Apply for Your Hermosa Beach Business License

Once your state filing is approved and your EIN arrives, you’re ready to apply for your Hermosa Beach business license. The city waives the first-year business license tax for most new businesses, which saves you several hundred dollars in year one according to Hermosa Beach Revenue Services. Apply online through the city’s licensing portal and submit your Commercial Business Application at the same time. The city also requires compliance with local regulations and SB 205 stormwater requirements, so submit the NPDES/SB 205 form with your license package. Tim Anhorn at Hermosa Beach Revenue Services handles licensing questions and can be reached at business_license@hermosabeach.gov or 310-318-0206. City Hall for in-person licensing is located at 1315 Valley Drive, open Monday through Thursday, 7 AM to 6 PM.

Coordinate Your Formation Timeline

The filing process moves quickly once you know where to go, but coordination matters. Your state formation documents, EIN, and local business license all work together to establish your legal presence. Getting these pieces in place before you launch operations prevents compliance gaps that create problems later. The next chapter covers the contracts and documentation you need to protect your business once these foundational filings are complete.

Contracts and Documentation You Need Before Launch

Your formation paperwork is filed, your EIN is approved, and your business license is hanging on the wall. Now comes the part that actually protects you when things go wrong. Operating agreements, bylaws, employment contracts, and vendor agreements are not optional paperwork to file away and forget. They define who owns what, how decisions get made, who handles money, and what happens if someone breaches a deal.

Without them, you face disputes that destroy young companies. We’ve seen founders skip this step and regret it within months when a co-founder disagrees on equity, an employee claims they were promised ownership, or a vendor refuses to deliver because the terms were never written down. The difference between a strong contract and a handshake agreement is the difference between enforcing your rights and losing money you can’t recover.

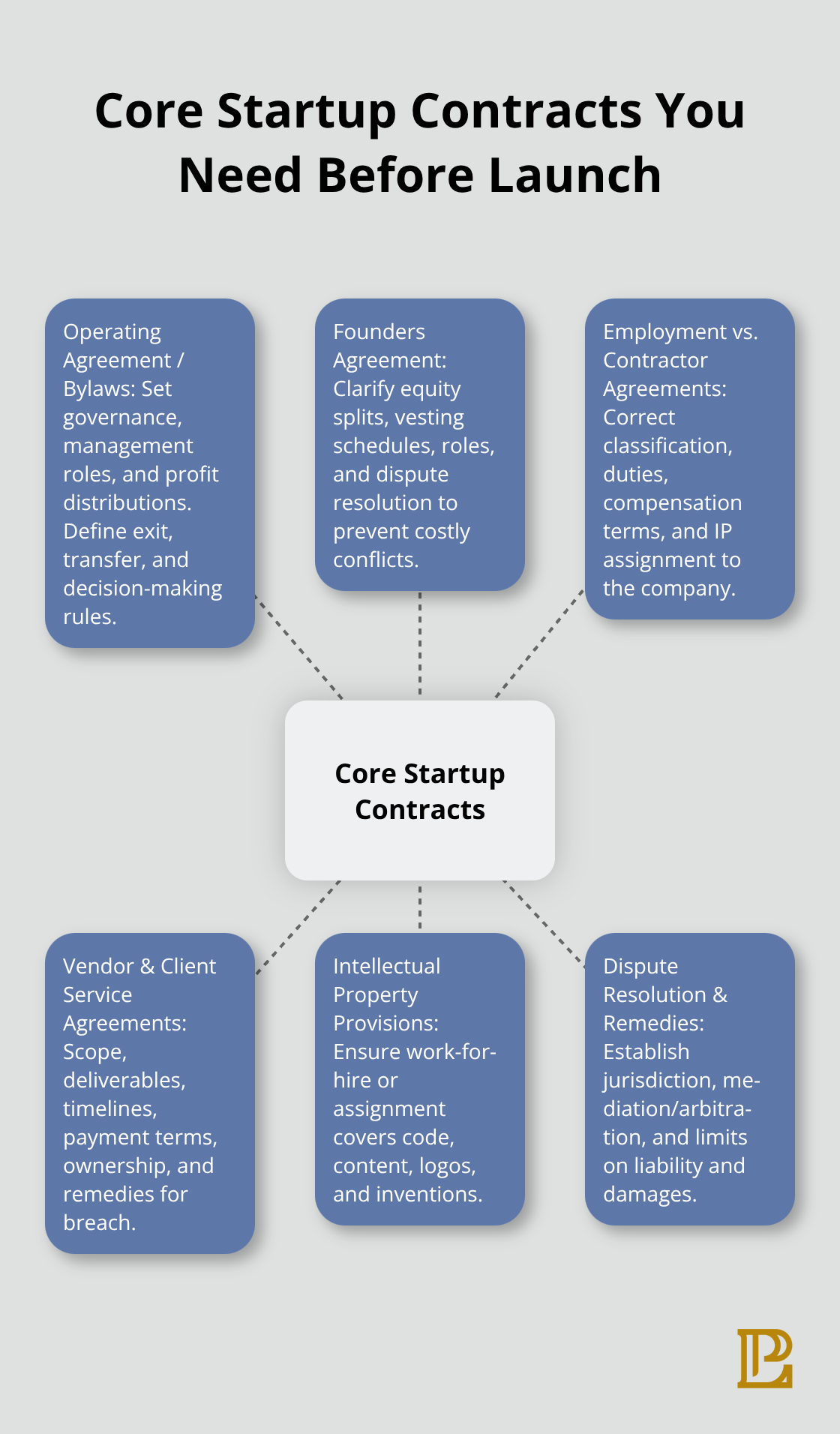

Operating Agreements and Bylaws Shape Your Business Structure

Start with your operating agreement if you formed an LLC. This document stays in your records and outlines how your business operates, who manages it, how profits split among owners, and what happens if an owner wants to leave or sell their stake. California law allows significant flexibility here, which means you can customize the agreement to your specific situation rather than defaulting to the state’s generic rules. If you incorporated instead of forming an LLC, bylaws serve the same function as an operating agreement and establish the corporate governance framework from day one.

Founders Agreements Prevent Equity Disputes

A founders agreement is critical if you have co-founders. It addresses ownership percentages, vesting schedules so equity doesn’t vest all at once, roles and responsibilities to prevent misalignment, and dispute resolution methods to avoid costly litigation if founders disagree. About 90 percent of California startups fail, and founders argue about control and equity far more often than they admit. Written vesting schedules prevent one founder from claiming full ownership if they leave after six months. These agreements protect all parties and clarify expectations before tensions arise.

Employment and Contractor Agreements Protect Your Payroll

California employment law is among the strictest in the country, and misclassifying someone as a contractor when they should be an employee creates wage-and-hour liability, unpaid payroll taxes, and penalties that compound quickly. Your agreement must clarify whether someone is an employee or contractor, define their duties, specify compensation and payment terms, and address intellectual property ownership so work products belong to your company rather than the individual. This distinction matters more than most founders realize.

Vendor and Client Service Agreements Lock Down Terms

Vendor and client service agreements protect you by putting the scope of work, deliverables, timelines, payment terms, and liability limits in writing. An oral agreement that a vendor will deliver a website in three months for five thousand dollars sounds clear until the vendor delivers late, the client refuses to pay, and you have no written proof of what was promised. Service agreements also specify who owns the work once it’s complete, what happens if either party breaches, and how disputes get resolved. These agreements take time to draft properly, but they cost far less than litigation to enforce an oral promise. Pierview Law handles contract drafting and entity formation together so your agreements align with your business structure and protect your interests from the start.

Final Thoughts

Hermosa Beach startup formation succeeds when you handle the legal foundation before problems emerge. The three decisions that matter most are your business structure, your formation documents, and your contracts. Choose an LLC if you want liability protection without double taxation, file your Articles of Organization through the Secretary of State, secure your EIN from the IRS, and apply for your Hermosa Beach business license to capture the first-year tax waiver that saves you hundreds of dollars.

The mistakes that derail startups happen early and quietly. Choosing the wrong entity structure costs you in taxes or leaves your personal assets exposed. Skipping a founders agreement creates equity disputes that split teams apart. Misclassifying employees as contractors triggers wage-and-hour liability that compounds with penalties, and operating without written vendor agreements means you have no recourse when someone fails to deliver.

Your next step is to work with a law firm that understands Hermosa Beach and the Los Angeles startup ecosystem. Pierview Law handles entity formation, contract drafting, and financing support so your business structure and agreements work together from day one. Reach out at 310-975-3183 or visit them at 2447 Pacific Coast Highway, 2nd Floor in Hermosa Beach.