Los Angeles corporate governance practices shape how companies operate, make decisions, and protect shareholder interests. Poor governance costs businesses money, damages reputation, and invites regulatory scrutiny.

At Pierview Law, we’ve seen firsthand how transparent governance structures prevent costly disputes and keep companies compliant. This guide walks you through the standards, systems, and strategies that matter most for your business.

What Governance Standards Apply to Your Los Angeles Corporation

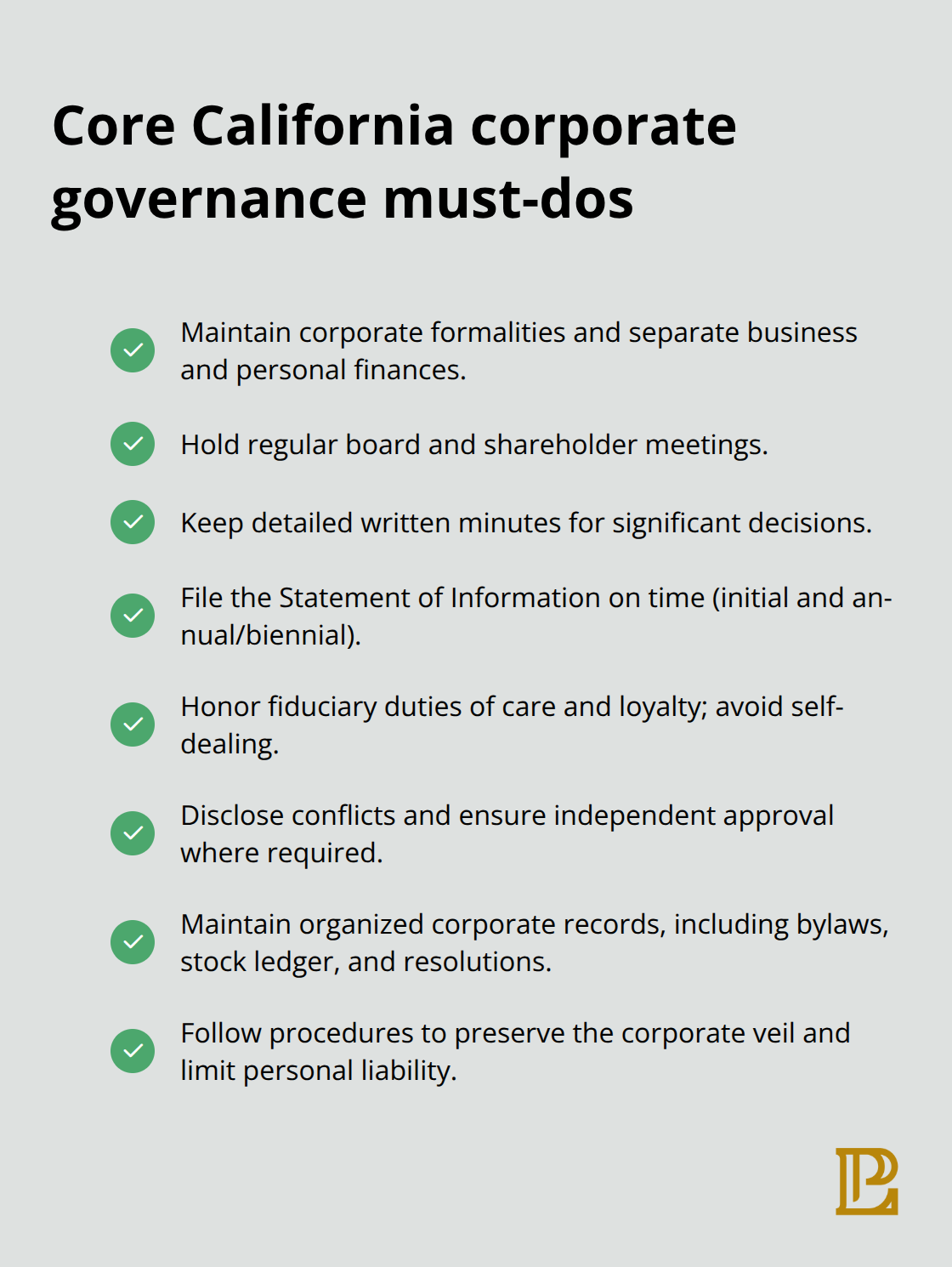

California law establishes clear governance requirements that every corporation must follow, and ignoring these standards invites personal liability for directors and officers. The California Corporations Code mandates that you maintain corporate formalities, keep separate finances, hold regular board and shareholder meetings, and document decisions in written minutes. If you fail to maintain these basics, courts can pierce the corporate veil and hold you personally responsible for company debts and liabilities. The State of California Secretary of State requires you to file a Statement of Information within 90 days of formation and then annually or biennially, with late-filing penalties ranging from fines to administrative dissolution.

You also owe fiduciary duties of care and loyalty to your shareholders-meaning your board decisions must be informed, transparent, and free of self-dealing. If you breach these duties, shareholders can sue you personally, and California courts take these violations seriously.

Regulatory Requirements That Directly Impact Your Bottom Line

California imposes an annual Franchise Tax minimum payment of $800 on corporations, with possible exemptions for some new corporations in their first year. Beyond taxes, you must comply with California’s employment laws, which impose strict wage, hour, break, and non-discrimination requirements through the California Department of Industrial Relations. Data privacy demands equal attention under the California Consumer Privacy Act and California Privacy Rights Act-if you handle personal information of California residents, you must provide clear privacy notices, honor consumer rights to access and delete data, and implement robust security measures. The California Transparency in Supply Chains Act applies if you are a retail seller or manufacturer doing business in California with annual worldwide gross receipts exceeding $100 million. This law requires you to post disclosures on your website covering verification, audits, certification, internal accountability, and training related to slavery and human trafficking in your supply chain. Companies that fail these disclosures face enforcement action from the California Attorney General.

Board Structure and Shareholder Accountability in Practice

Your board composition matters more than many owners realize. Directors must have the knowledge and independence to oversee company strategy, financial reporting, and risk management without conflicts of interest. Shareholders retain the right to vote on directors and major corporate actions, inspect certain company records, and receive pro-rata dividends if declared. You must hold board and shareholder meetings at least once per year, and you must maintain meticulous minutes documenting every significant decision, election, and resolution. These records prove you acted in good faith and followed proper procedures-they are your best defense if a shareholder later challenges a board decision. Many Los Angeles companies skip this step or treat minutes as an afterthought, then face disputes later when someone questions whether a decision was properly authorized.

Why Documentation Protects You and Strengthens Your Company

Governance documentation serves as your shield against personal liability and your proof of legitimacy to lenders, investors, and regulators. When you maintain clear records of board actions, shareholder votes, and management decisions, you demonstrate that your company operates with integrity and follows the law. Courts and regulators view well-documented governance as a sign of a serious, professionally managed business. Weak or missing documentation, by contrast, raises red flags and invites scrutiny. The cost of creating and maintaining proper records is minimal compared to the cost of litigation, regulatory fines, or personal liability exposure. Your next step involves building the internal systems and decision-making processes that make transparent governance work in practice.

How to Build Decision-Making Systems That Actually Work

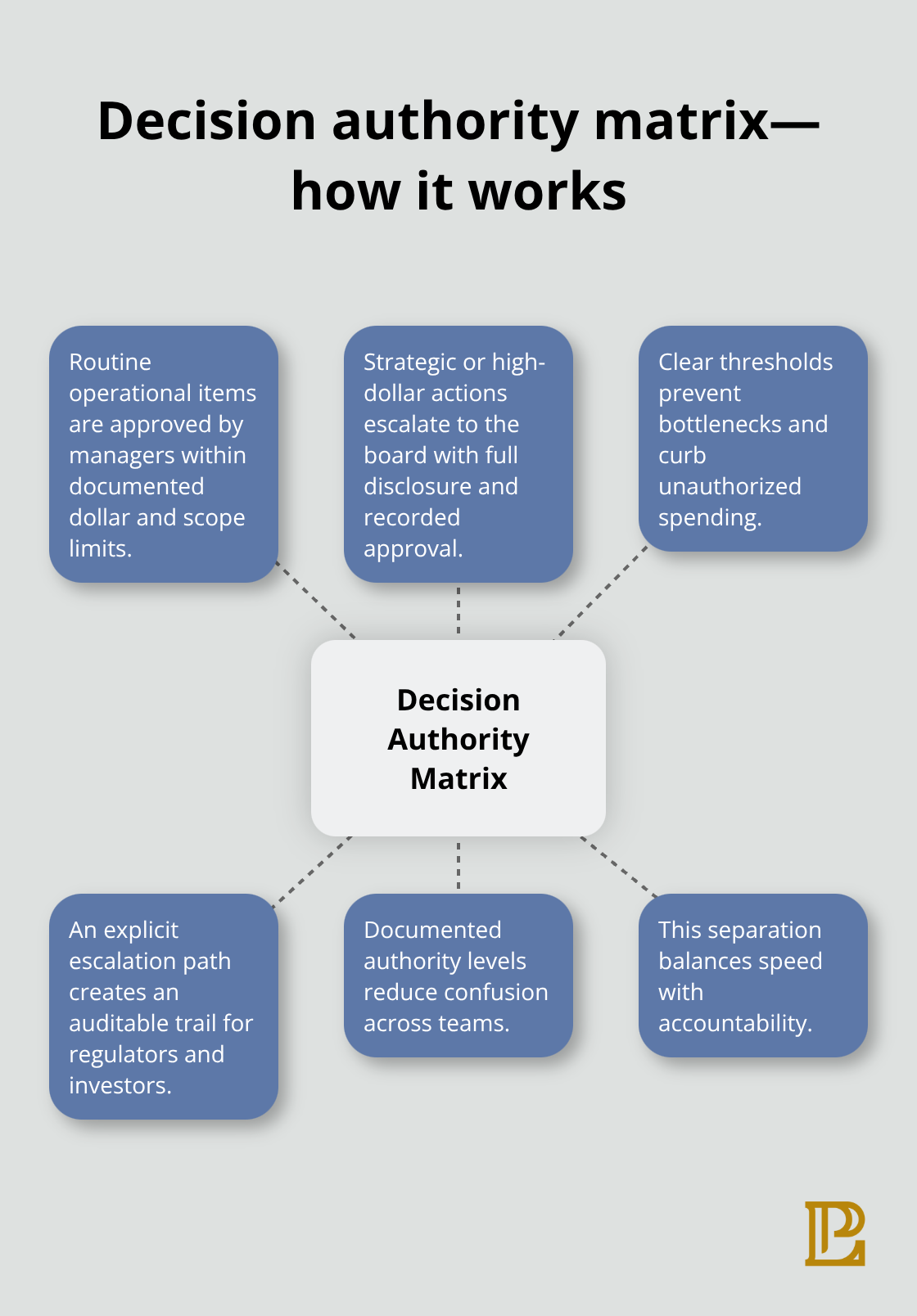

Transparent governance requires more than annual meetings and signed documents. You need operational systems that embed good decision-making into your company’s daily routines. The most effective approach separates routine operational decisions from major strategic and financial decisions, then assigns clear authority for each category.

Establish Clear Authority Levels for Different Decision Types

Routine decisions-such as hiring below a certain salary level, purchasing supplies under a dollar threshold, or scheduling routine maintenance-should go to management with documented approval limits. Strategic decisions-such as mergers, acquisitions, material contracts above a set amount, equity issuance, dividend declarations, or major capital expenditures-must go to the board with full disclosure and documented board approval. This separation prevents bottlenecks while preserving accountability.

Create a written decision authority matrix that spells out who can approve what amount and what type of decision, then distribute it to all managers. When a decision falls within a manager’s authority, they execute it. When it exceeds that authority, it escalates to the board. This system reduces confusion, prevents unauthorized spending, and creates an audit trail that regulators and investors can review.

Without this structure, you end up with either decision paralysis-where nothing moves without board approval-or rogue decisions made without proper oversight.

Document Your Board Decisions With Substance, Not Just Formality

Documentation transforms good intentions into enforceable governance. The California Corporations Code requires that board and shareholder meeting minutes document the decisions made, who voted, and whether the vote was unanimous or split. Many Los Angeles companies treat minutes as a formality, recording only bare facts like attendance and approval of last month’s minutes.

Instead, your minutes should capture the business rationale behind each decision-why the board approved a contract, what risks the board discussed, what alternatives the board considered, and what information the board relied upon. This detail protects directors if a shareholder later sues, because courts assume directors acted in good faith when they document their reasoning. Additionally, maintain a corporate records binder that includes your Articles of Incorporation, bylaws, stock ledger, meeting minutes, board resolutions, and major contracts. Store this physically and digitally in a secure location accessible to authorized personnel.

Organize Your Compliance Calendar to Avoid Costly Penalties

When you apply for a loan, attract investors, or face a regulatory inquiry, organized records demonstrate professional management and reduce friction in due diligence. Establish an annual compliance calendar that reminds you when to file your Statement of Information with the California Secretary of State, when to pay your Franchise Tax, when to hold annual shareholder and board meetings, and when to renew licenses and permits.

Missing these deadlines costs money-late Statement of Information filings trigger penalties, and the California Secretary of State can administratively dissolve your corporation if you fall behind. Assign one person responsibility for this calendar and hold them accountable. The cost of staying organized is negligible compared to the cost of losing your corporate status or facing personal liability because governance formalities were ignored.

Once you establish these decision-making systems and documentation practices, you face the reality that governance does not operate in a vacuum. Your board and management must navigate competing interests from shareholders, employees, customers, and regulators-and conflicts of interest often emerge in these situations.

Where Governance Conflicts Hurt Your Bottom Line

Los Angeles companies face real pressure when shareholders, employees, lenders, and regulators want different things from your business. A shareholder might push for maximum distributions while a lender’s covenants require you to retain earnings. An employee wants job security while an investor demands cost cuts to improve margins. Your board must navigate these competing demands without freezing decision-making or exposing the company to liability.

How Conflicts of Interest Emerge in Real Governance Situations

Conflicts arise when a director votes on a transaction where they have a financial stake, when management pushes a decision that benefits them personally over shareholder value, or when a major shareholder demands preferential treatment that disadvantages minority shareholders. The practical reality is that conflicts surface regularly in governance, and how you handle them determines whether your company maintains credibility with stakeholders or faces disputes that drain resources and damage relationships.

California law requires directors to disclose conflicts and either recuse themselves from the vote or demonstrate that the conflicted transaction was entirely fair to the company. Many Los Angeles business owners underestimate how seriously courts take these violations. If a shareholder proves that a director engaged in self-dealing without proper disclosure and board approval, that director faces personal liability and the company may recover damages.

Building a Conflict Register That Actually Works

Your board should maintain a conflict-of-interest register where directors disclose financial interests, family relationships, and business dealings that could affect their judgment. Before each board meeting, review this register and identify which agenda items might trigger conflicts. If a conflicted director participates in a vote anyway, document that they abstained or were recused, and ensure the remaining directors voted with full knowledge of the conflict.

This transparency does not eliminate conflicts, but it demonstrates that your board acted in good faith and followed proper procedures. When you document how conflicts were handled, you create a record that protects both the company and individual directors if disputes arise later.

Staying Ahead of Regulatory Changes That Affect Your Operations

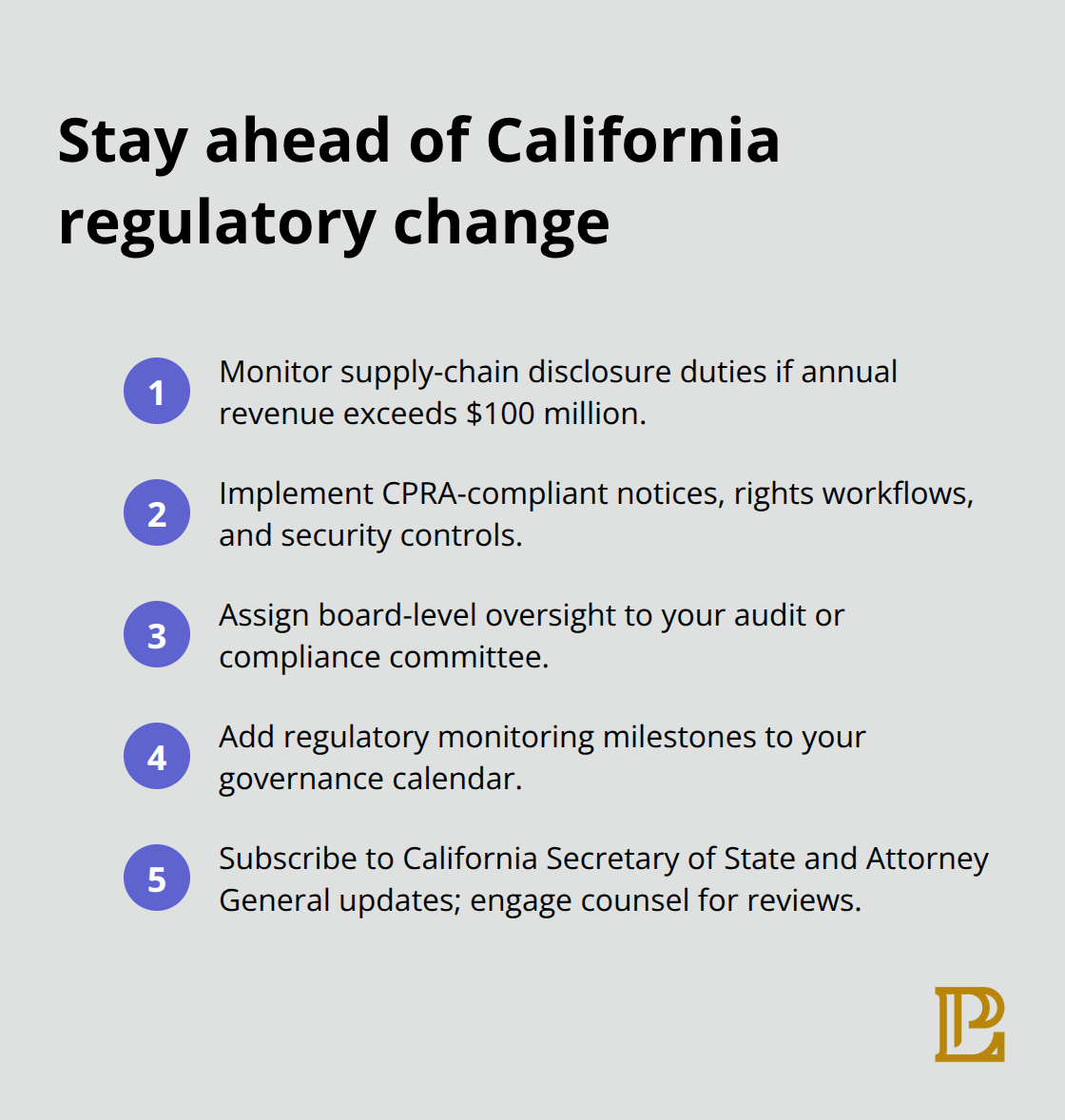

Regulatory requirements in California and beyond shift constantly, and your governance structure must adapt without becoming rigid or reactive. The California Transparency in Supply Chains Act requires companies with over $100 million in annual revenue to post disclosures about slavery and human trafficking prevention in their supply chains, and the California Attorney General actively enforces this requirement. The California Privacy Rights Act imposes strict rules on how you collect, use, and protect personal data from California residents, with penalties reaching thousands of dollars per violation.

Federal securities laws, if your company raises capital from institutional investors, impose additional disclosure and governance obligations. Rather than treating compliance as a checklist, embed regulatory monitoring into your governance calendar and assign board-level oversight to your audit or compliance committee. Subscribe to updates from the California Secretary of State and California Attorney General, and engage legal counsel to review changes that affect your industry and business model.

Why Proactive Compliance Costs Less Than Reactive Enforcement

Many governance failures stem not from willful violations but from ignorance that a new rule applies to your company. A manufacturer with $110 million in revenue might not realize the Transparency in Supply Chains Act applies to them, then face enforcement action when the California Attorney General discovers missing disclosures. A technology company might overlook California Privacy Rights Act requirements because they focus on federal compliance.

Your board should schedule quarterly governance updates to discuss regulatory changes, assess whether new rules affect your operations, and authorize management to implement necessary changes. This approach costs less than reactive compliance and keeps your company ahead of regulatory risk. Proactive counsel helps you identify emerging obligations before regulators identify gaps in your compliance.

Final Thoughts

Transparent governance shapes how your Los Angeles corporation makes decisions, manages risk, and builds trust with shareholders, lenders, and regulators. Maintain corporate formalities, document your decisions with substance, establish clear authority levels for different decision types, and stay ahead of regulatory changes. When you separate routine operational decisions from strategic board-level decisions, you create accountability without paralysis.

Los Angeles corporate governance practices must adapt to California’s evolving regulatory landscape. The Transparency in Supply Chains Act, California Privacy Rights Act, and Franchise Tax requirements are not optional, and missing these deadlines costs money while inviting regulatory scrutiny. Build a compliance calendar, assign clear responsibility for each deadline, and subscribe to updates from the California Secretary of State and California Attorney General to catch regulatory shifts before they affect your operations.

Companies with strong governance attract capital more easily, retain talented employees who value integrity, and build customer loyalty through demonstrated accountability. If you operate a business in Hermosa Beach or elsewhere in Los Angeles County and need guidance building or strengthening your governance structure, Pierview Law provides personalized legal services in business law, entity formation, and corporate governance. Schedule a consultation to assess your current governance practices and identify gaps that need attention.