A property title review in California isn’t optional-it’s the foundation of any smart investment. Without it, you risk inheriting someone else’s legal problems, from hidden liens to boundary disputes that could cost you thousands.

At Pierview Law, we’ve seen investors skip this step and regret it. This checklist walks you through exactly what to examine before you commit your money.

What You’re Actually Looking For in Title Records

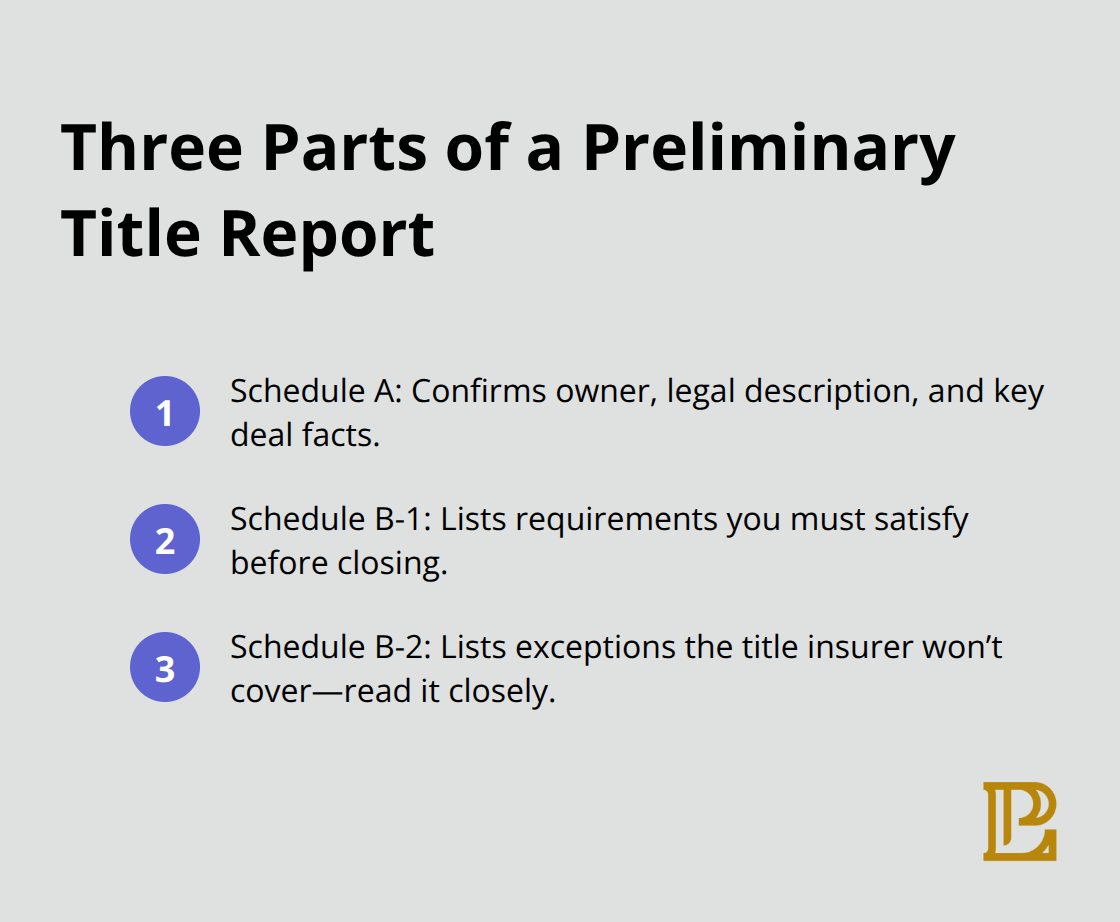

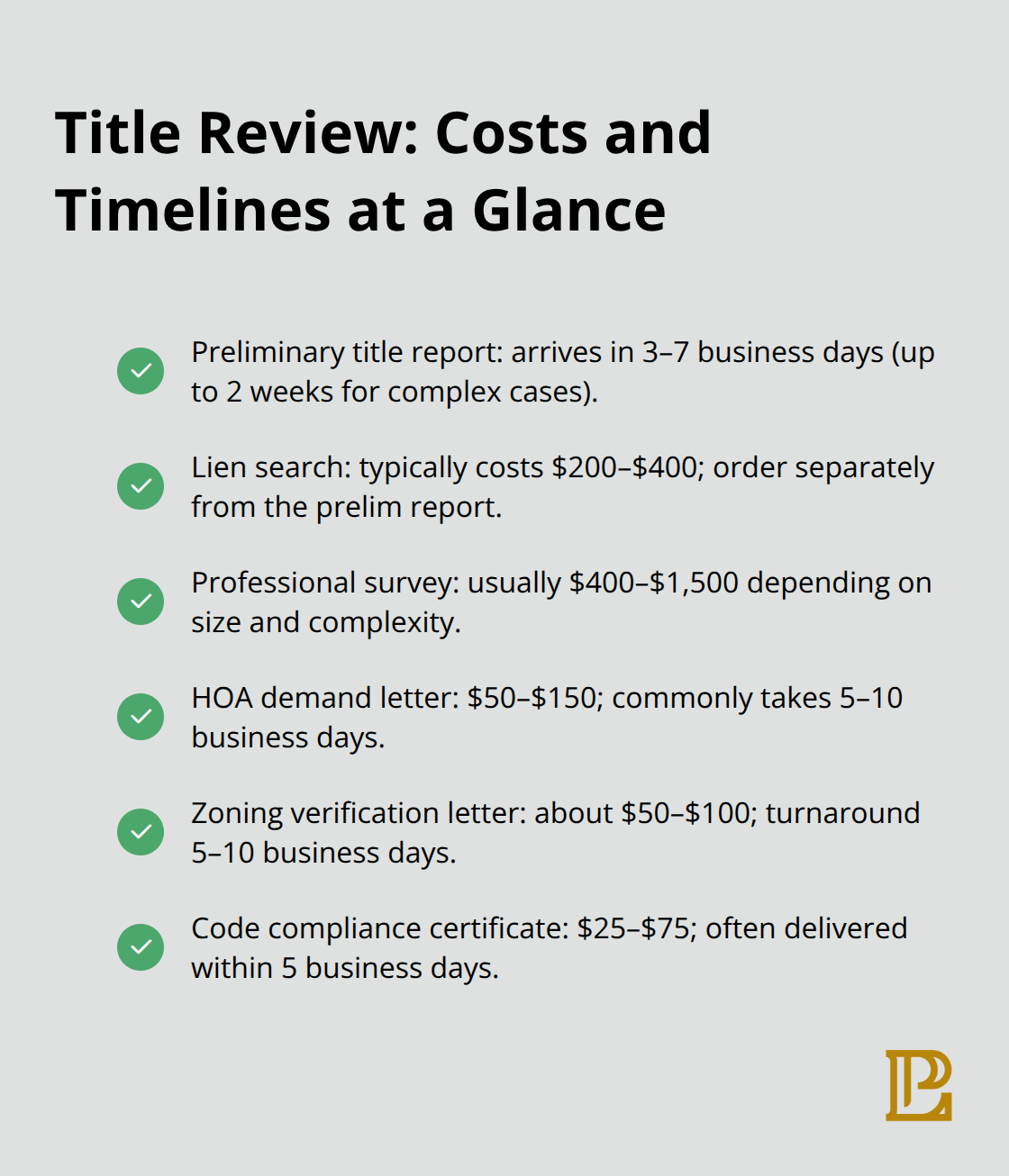

A property title review means systematically examining every recorded document tied to a property to confirm who owns it, what debts attach to it, and what restrictions limit how you can use it. This isn’t about reading a title report passively-it’s about understanding what each line means and what it costs you. Start with the preliminary title report from a title company, which shows the current owner, any mortgages or liens, easements, and items the title insurer won’t cover. This report typically arrives within 3 to 7 business days after escrow opens, sometimes up to 2 weeks for complex properties. The report contains three key sections: Schedule A lists basic facts like the current owner and sales price; Schedule B-1 shows requirements you must satisfy before closing, such as clearing a lien; and Schedule B-2 lists exceptions-issues the title policy won’t protect you against. Read Schedule B-2 carefully. Many investors skip it and later discover they’ve accepted restrictions on their property that limit future development or resale value.

Uncovering Hidden Debts and Claims

Public records contain liens, judgments, and tax claims that directly impact your ability to refinance or sell. A property tax lien in California gets filed by the county if property taxes go unpaid, and these liens have priority over most other claims, meaning they get paid first if the property is sold. Mechanic’s liens from contractors or suppliers who weren’t paid also appear in public records and can delay closing by weeks. Order a lien search specifically-don’t rely solely on the preliminary title report-because unrecorded liens sometimes surface later. Judgments from court cases attach to a property if the owner lost a lawsuit, and these show up in county records under the owner’s name. A title company search typically costs between $200 and $400 and covers recorded liens, but you should also ask your title company or attorney to flag any judgments against the current owner that might transfer to you. HOA liens are particularly common in Hermosa Beach and throughout Los Angeles County; if an owner owes homeowners association fees, the HOA can place a lien on the property, and you could inherit that debt at closing if it isn’t paid off first.

Boundary and Description Accuracy

The legal description on the deed must match the actual land boundaries, and mismatches can torpedo a deal or create expensive disputes later. Order a current professional survey from a licensed surveyor-not an old one from 10 years ago-because property lines can be reestablished or clarified over time, and lenders increasingly require updated surveys before funding. A survey costs $400 to $1,500 depending on property size and complexity, but it’s far cheaper than a boundary lawsuit. Compare the surveyed boundaries against the recorded plat map and the legal description in the preliminary title report. If the survey shows the building encroaches on neighboring land or if the recorded description doesn’t match the physical parcel, the title company must correct it before issuing a policy, or you must accept the risk and move forward with a title exception. In Hermosa Beach, where many properties sit coastal or near fault lines, surveyors often flag easements for utilities or public access that weren’t obvious from the deed alone.

What Comes Next in Your Review

Once you’ve examined the preliminary title report, ordered your lien search, and obtained a current survey, you’re ready to move into the next phase of your title review. The documents you’ve gathered now form the foundation for checking zoning compliance, HOA restrictions, and code violations-each of which can significantly affect your investment’s value and your ability to use the property as intended.

Title Problems That Cost Investors Real Money

Tax Liens and Mortgage Debt

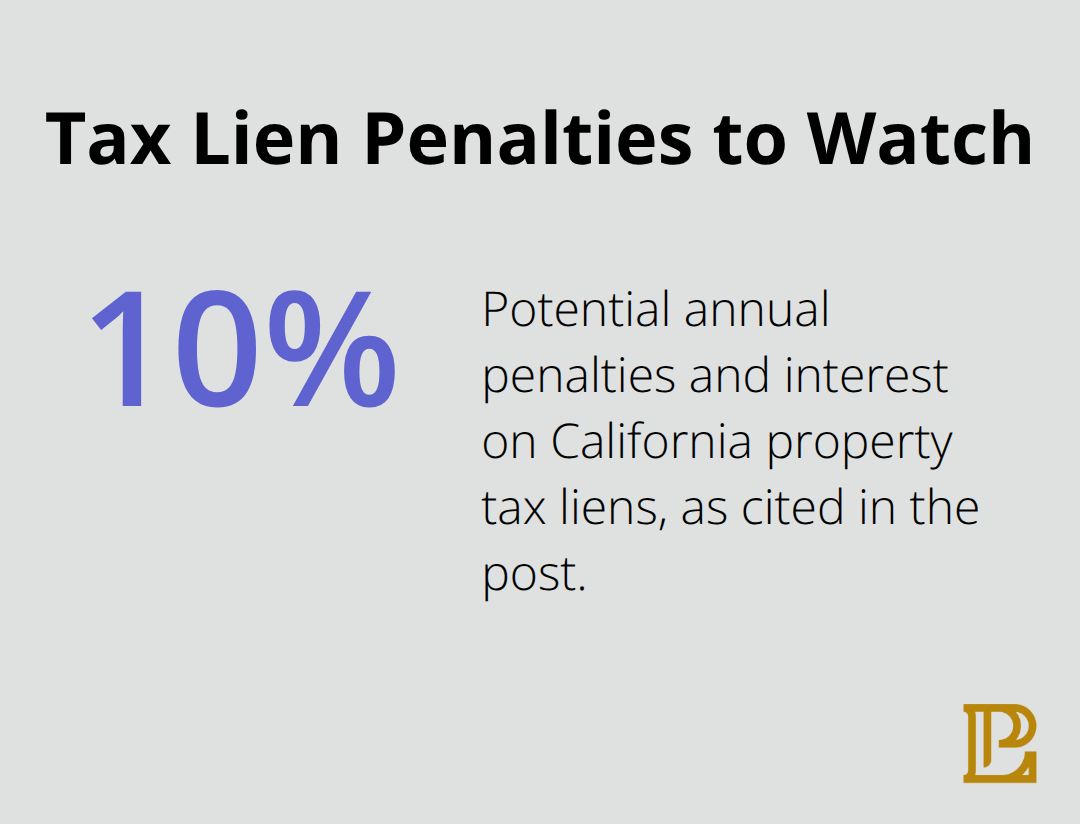

Tax liens and mortgage debt represent the most immediate threat to your investment timeline and closing date. California counties file property tax liens automatically when taxes go unpaid for even one year, and these liens take priority over nearly every other claim against the property. When the property sells, the county gets paid first before any other creditor. Tax liens accrue penalties and interest that compound monthly, sometimes reaching 10 percent annually under California Revenue and Taxation Code Section 2701. When you review the preliminary title report, you’ll see these liens listed under Schedule B-1 as items requiring payment before closing.

Mortgage liens from the current owner’s lender also appear on the report, and while the seller typically pays these off at closing from sale proceeds, you must verify the payoff amount matches what the lender confirms in writing.

Mechanic’s Liens and HOA Claims

Mechanic’s liens from unpaid contractors or suppliers create a different problem: they can appear in public records months after work is supposedly complete, and title companies sometimes hold back funds in escrow to cover potential mechanic’s liens that surface after closing. A title company lien search costs $200 to $400 and should always be ordered separately from the preliminary title report, because unrecorded liens occasionally emerge later and can cloud your ownership. HOA liens in Hermosa Beach properties are extremely common and frequently overlooked. If the current owner owes homeowners association fees, the HOA can place a lien against the property, and you’ll inherit that debt at closing unless it’s cleared first. Request an HOA demand letter showing the exact payoff amount needed to clear any lien, and never assume verbal assurances from the seller about unpaid fees.

Easements and Forged Documents

Easements and forged documents in the chain of title present subtler but equally serious risks that many investors underestimate. Easements for utilities, drainage, or public access appear on your preliminary title report under Schedule B-2, and while utility easements are typically harmless, access easements affecting driveways, views, or buildability require careful scrutiny because they can restrict how you develop or use the land. A professional survey will reveal easement locations and boundaries that don’t always appear clearly in written descriptions. Surveyors in Hermosa Beach frequently identify utility easements or coastal access rights that weren’t obvious from the deed alone.

Fraudulent or forged documents in a property’s ownership history are rare but devastating when they occur. They surface through title searches that reveal gaps in the chain of title or documents that don’t match county records. If the preliminary title report flags missing deeds, name changes that weren’t properly recorded, or signatures that don’t match prior documents, the title company must resolve these discrepancies before issuing a policy. Request copies of all deeds and transfers going back at least 30 years, and compare signatures and notary information across documents to spot inconsistencies. Title insurance protects you against undiscovered forged documents or fraudulent transfers, but only if you obtain a policy at closing. The policy typically costs 0.6 percent of the purchase price in California and covers claims that emerge years later.

Moving Forward With Your Title Review

Unresolved exceptions or clouds on title don’t disappear at closing-they transfer to you, and clearing them later becomes exponentially more expensive and time-consuming. Once you’ve identified these common problems through your preliminary title report and lien searches, you’re ready to move into the practical steps of your title review checklist, starting with ordering the right documents and understanding what each one reveals about your property’s legal standing.

Getting Your Title Documents in the Right Order

Order a Preliminary Title Report Before You Commit

Contact a title company in Los Angeles County as soon as you identify a property you’re serious about, even before you formally submit an offer. A preliminary title report costs nothing and arrives within 3 to 7 business days, sometimes up to 2 weeks for properties with complex ownership histories. Request the report early because title issues discovered after you’ve committed funds force renegotiations or kill the deal entirely. The preliminary title report shows the current owner, the property’s legal description, any mortgages or liens, easements, and covenants. Schedule A lists basic facts like the current owner and sales price. Schedule B-1 lists items you must clear before closing, such as unpaid property taxes or a mechanic’s lien. Schedule B-2 lists exceptions the title insurer won’t cover, meaning you accept those risks when you take ownership. Many investors skip Schedule B-2, but this section determines what restrictions or claims you’re inheriting. If an easement affects your ability to build or if an HOA lien hasn’t been cleared, Schedule B-2 reveals it.

Obtain a Current Professional Survey

Once you have the preliminary report, obtain a professional survey from a licensed surveyor. A current survey costs $400 to $1,500 depending on parcel size and complexity, but it’s mandatory for most lenders and essential for identifying boundary discrepancies or encroachments. Surveyors in Hermosa Beach frequently uncover utility easements, coastal access rights, or drainage restrictions that the deed doesn’t describe clearly. Compare the surveyed boundaries against the legal description in the preliminary title report and the recorded plat map. If the survey reveals the structure sits outside recorded boundaries or if easements restrict buildable area, the title company must resolve these issues before issuing a policy.

Verify HOA Restrictions and Outstanding Fees

HOA restrictions and covenants appear in the preliminary title report but require separate verification through an HOA demand letter. Request this letter directly from the homeowners association showing any outstanding fees, liens, or special assessments. The letter typically costs $50 to $150 and arrives within 5 to 10 business days. An HOA lien in California can reach thousands of dollars and transfers to you at closing if unpaid, making this step non-negotiable for any Hermosa Beach property in a planned community.

Check Zoning Compliance and Land Use Restrictions

Verify zoning compliance and land use restrictions through the City of Hermosa Beach Planning Department or the Los Angeles County assessor’s office. Use the Zone Information and Map Access System from City Planning to check whether the property’s current or intended use complies with zoning classifications. A property zoned for single-family residential cannot legally operate as a commercial office or short-term rental without a variance or conditional use permit. Request the zoning verification letter directly from City Planning, which costs $50 to $100 and takes 5 to 10 business days.

Confirm No Outstanding Code Violations

Confirm there are no outstanding code violations or permit issues by requesting a code compliance certificate from the local building department. This certificate verifies that all structures on the property meet current code standards and that no violations remain unresolved. Building departments in Los Angeles County charge $25 to $75 for this document and typically respond within 5 business days. If violations exist, the seller must resolve them before closing, or you must negotiate a credit to cover remediation costs.

Final Thoughts

A property title review in California protects your investment by identifying problems before they become your responsibility. Without this review, you inherit liens, boundary disputes, easements, and code violations that cost thousands to resolve after closing. The preliminary title report, survey, HOA verification, zoning check, and code compliance certificate form a complete picture of what you’re actually buying.

Take action on any issues the documents reveal. If the preliminary title report lists liens under Schedule B-1, confirm the seller will clear them at closing. If the survey shows boundary discrepancies, work with the title company to resolve them before you sign. If the HOA demand letter shows outstanding fees, negotiate a credit or require payoff at closing (and if zoning or code violations exist, decide whether remediation costs justify moving forward or whether you should walk away).

Property title review in California often requires professional guidance when issues become complex. Forged documents, missing deeds, or competing claims on the property demand legal intervention to resolve cleanly, and boundary disputes involving neighboring properties or easements that restrict development need attorney review to understand your actual rights. Contact Pierview Law to discuss your title review and move forward with a clear legal foundation for your real estate investment.